Executive Summary

This report explores the U.S. shampoo market in 2026, including consumer trends, scalp care demand, damage repair, textured-hair opportunities, price architecture, channel strategy, compliance boundaries, and OEM launch planning. It is designed to help brands, distributors, importers, and e-commerce sellers turn market insight into a more practical shampoo launch strategy.

U.S. Shampoo Market 2026: Consumer Trends, Scalp Care, and Product Opportunities

The U.S. shampoo market in 2026 remains one of the largest and most routine-driven categories in personal care, but it is no longer led by generic cleansing alone. The market is being reorganized around targeted need states such as scalp balance, damage repair, color maintenance, moisture retention, buildup removal, and density-support positioning.

For brands, importers, distributors, and e-commerce sellers, this creates a different type of opportunity. Shampoo is still a high-frequency purchase, but the winning products are no longer the ones that simply say “cleanses hair.” The strongest launches are built around visible outcomes, clear need-state positioning, and channel-fit execution.

This report translates category signals into product and launch logic. It covers consumer demand, competitive structure, price tiers, product opportunity mapping, compliance boundaries, and OEM-ready development strategy for the U.S. shampoo market in 2026.

Executive Summary

The U.S. shampoo market is still a high-volume category, but it is no longer growing through broad “for all hair types” positioning. Instead, demand is concentrating around more specific product territories: scalp health, damage repair, color-safe maintenance, moisture-first cleansing for textured hair, clarifying without stripping, and volume or density-support routines.

This matters because shampoo is no longer just the cleansing step. It has become the first treatment touchpoint in the consumer routine. Shoppers increasingly expect shampoo to help solve a real problem, whether that problem is oily roots, buildup, dryness, breakage, flaking, faded color, or weak-looking hair.

For most new entrants, the most commercially efficient first SKU is a sulfate-free scalp and damage balance shampoo in the masstige tier. It is broad enough for strong audience fit, premium enough to support healthier margins, and structured enough to work across Amazon, DTC, and selective retail.

Market Opportunity Overview

The U.S. shampoo market in 2026 is defined less by category expansion alone and more by benefit migration. Consumers are shifting from basic cleansing toward problem-solving cleansing. That shift is changing how shampoo should be developed, merchandised, and priced.

Shampoo remains the anchor product in U.S. hair care and still serves as the entry point for both mass and premium regimens. In many cases, it is the first product a consumer uses to try a new brand. That makes it a traffic-driving SKU as well as a retention-driving SKU.

The most commercially attractive growth zones are:

- scalp-led care

- anti-dandruff and itch-relief positioning

- bond-repair and damage-repair systems

- color-safe maintenance

- moisture-retention cleansing for curls, coils, and textured hair

- clarifying formats that clean effectively without leaving hair stripped

The strongest opportunities sit where performance, sensory payoff, and benefit clarity meet.

Market Direction: Five Transformative Shifts

What Is Driving Demand in 2026

Several structural shifts are shaping the market.

The first is scalp care becoming mainstream. Consumers are increasingly concerned with buildup, itch, dryness, visible flakes, root oiliness, and overall scalp comfort. This has moved scalp-coded shampoo from niche territory into a broader, more commercially relevant space.

The second is premiumization with proof. Consumers will pay more for repair, scalp outcomes, color maintenance, and salon-coded results, but they are less willing to pay simply for vague botanical storytelling or generic clean beauty language.

The third is channel hybridization. A shampoo now has to work across shelf and screen. It must photograph well online, communicate benefits quickly, ship safely, and still perform strongly enough to drive repeat purchase.

The fourth is the decline of weak differentiation. Sulfate-free has become a baseline expectation in many segments. It still matters, but it is no longer enough to carry the full product story on its own.

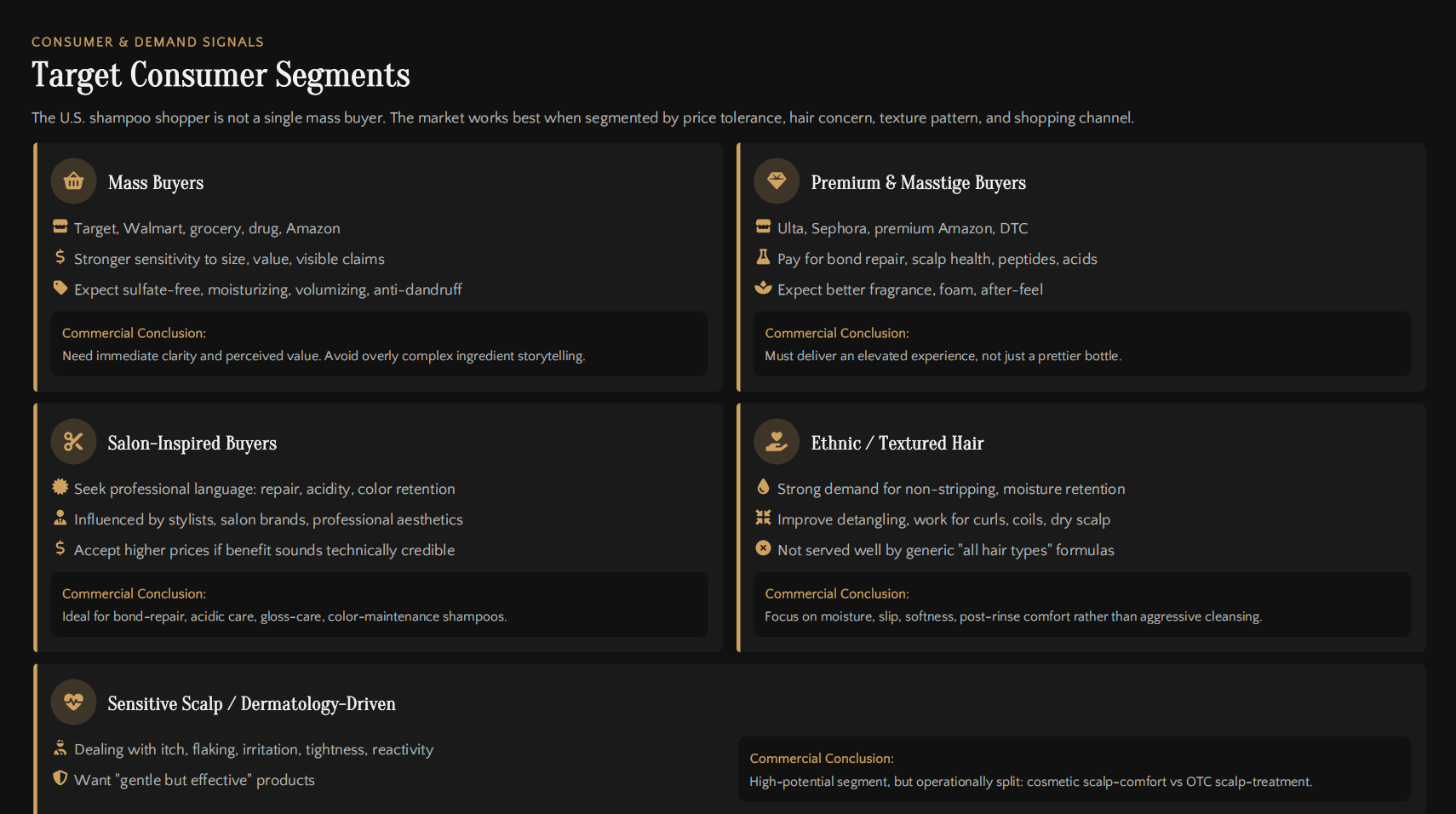

Consumer Demand Signals

The U.S. shampoo buyer is not a single mass-market shopper. The category works best when segmented by concern, price tolerance, hair texture, and channel behavior.

The strongest need states include:

- oily roots and scalp buildup

- dandruff, itching, and visible imbalance

- color-treated and heat-damaged hair

- dry, curly, coily, or textured hair needing moisture retention

- fine, flat, or density-concern hair

- clarifying reset needs related to styling products, hard water, or frequent washing

Consumers are also shopping more consciously by use case. They are not just buying “a shampoo.” They are buying a daily scalp balance shampoo, a moisture shampoo for curls, a clarifying reset shampoo, or a repair shampoo for damaged hair.

This shift favors brands that define one strong problem and solve it clearly.

Target Consumer Segments

Key Purchase Drivers

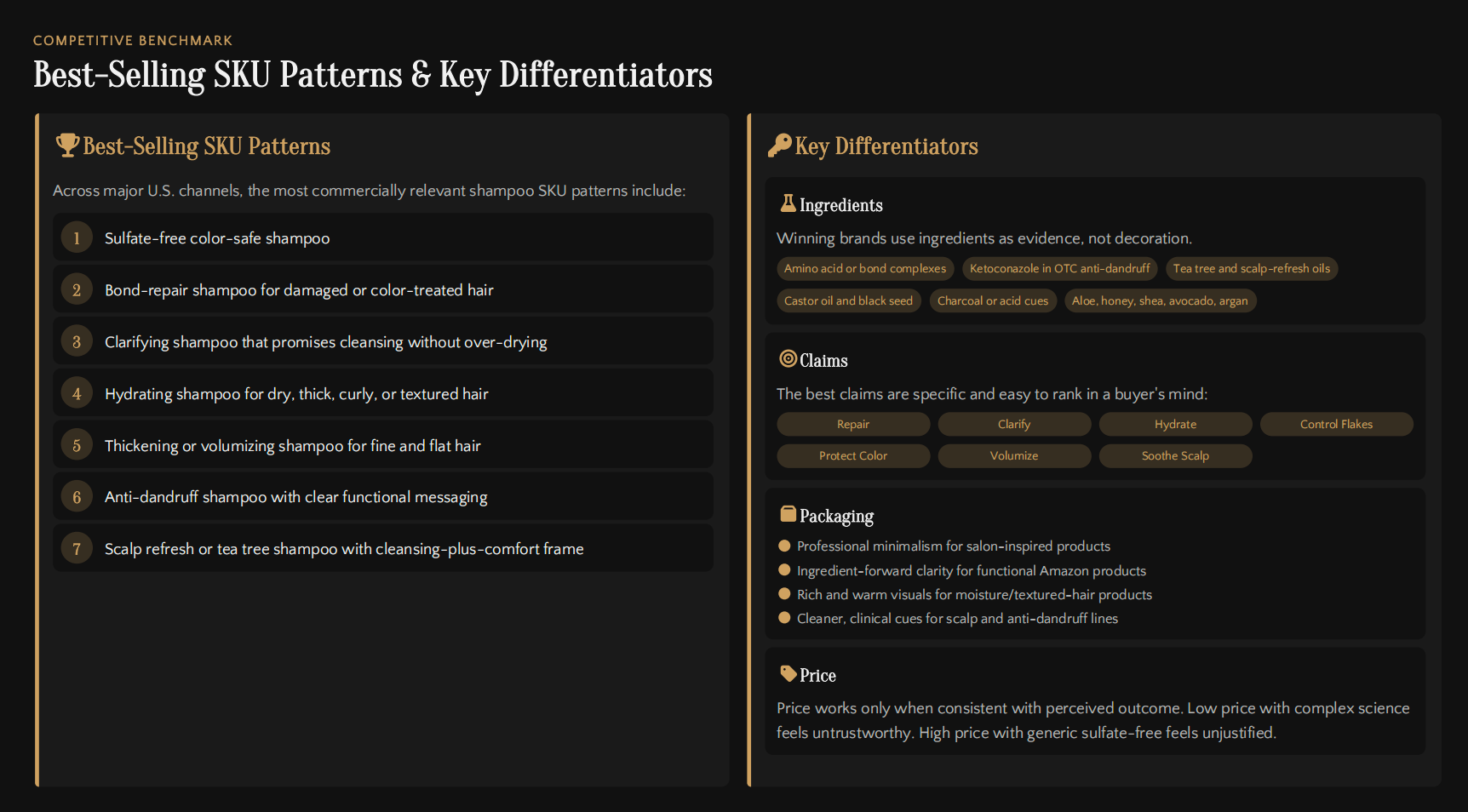

Several factors now drive conversion more strongly than broad ingredient storytelling alone.

The first is benefit clarity. The product must make its purpose obvious at first glance. Claims such as scalp balance, damage repair, moisturizing, clarifying, color-safe, and thickening remain easier to understand and easier to shop.

The second is sensorial performance. Shampoo is tactile commerce. Foam quality, rinse feel, fragrance, scalp comfort, and after-wash softness directly affect repeat purchase.

The third is ingredient logic. Consumers still look for sulfate-free systems, bond-building language, peptides, scalp-refresh cues, and moisturizing oils, but these ingredients work best when connected to a visible performance promise.

The fourth is price-to-experience alignment. A premium price must feel earned through formula behavior, fragrance, packaging, and post-rinse result.

The Most Commercially Relevant Product Directions

The strongest U.S. shampoo opportunities in 2026 are not generic “clean” or “natural” products. They are clearly defined product territories with strong commercial logic.

High-potential directions include:

- scalp balance daily shampoo for oily roots and buildup

- bond repair shampoo for damaged or color-treated hair

- clarifying moisture reset shampoo

- moisture-retention shampoo for curls, coils, and textured hair

- sensitive scalp comfort shampoo

- thickening or volume-support shampoo

- anti-dandruff shampoo developed through a proper OTC route

- color-protect gloss shampoo

Each of these directions maps to a distinct consumer problem, which makes them easier to position, easier to search, and easier to expand into a broader line architecture.

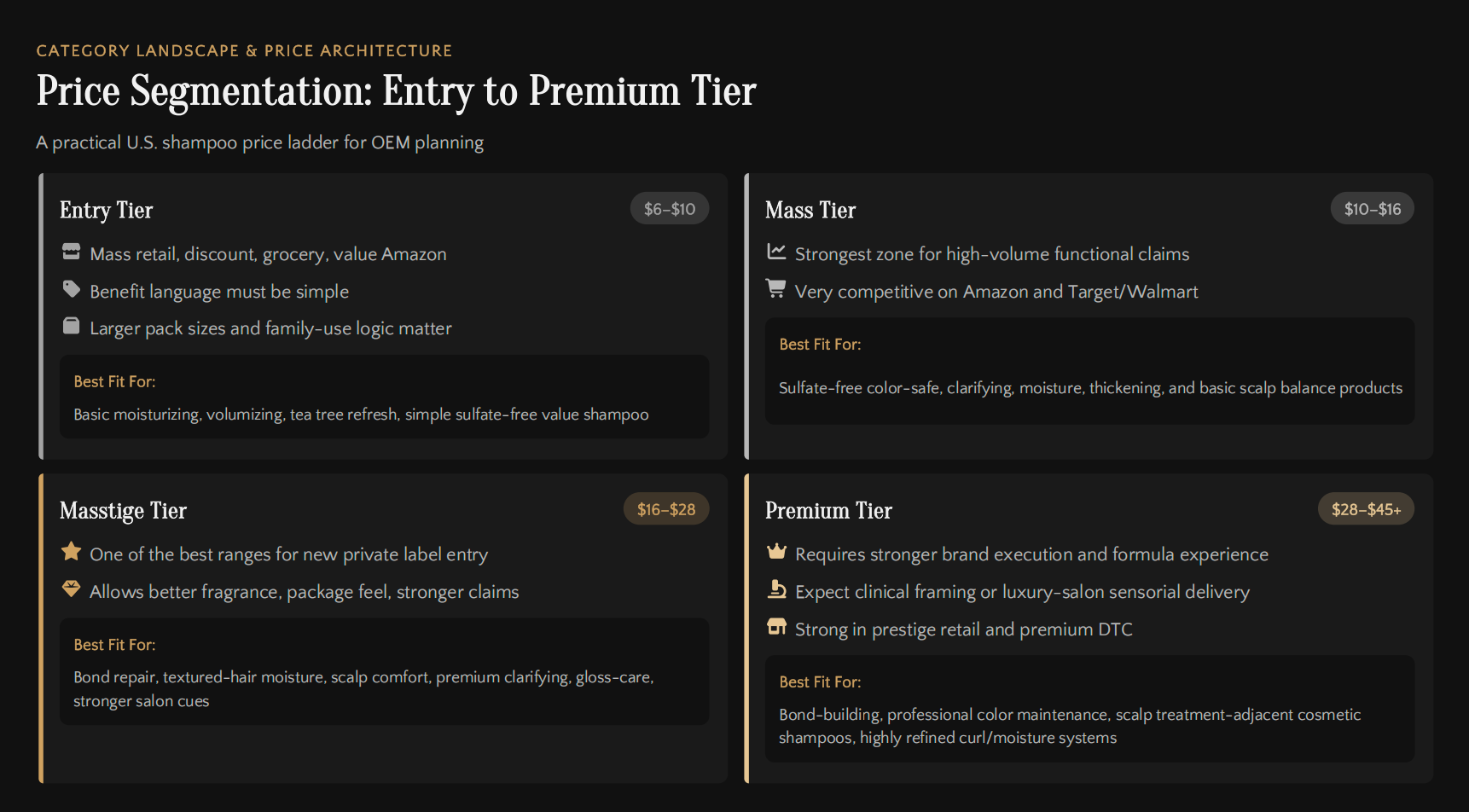

Price Band Strategy

A practical U.S. shampoo price ladder in 2026 can be divided into four main zones.

Entry tier products compete on affordability, size, and direct clarity. These are suitable for basic moisturizing, simple sulfate-free cleansing, and family-use positioning.

Mass tier products remain highly competitive and work best for sulfate-free color-safe, clarifying, moisturizing, and thickening products with strong shelf readability.

Masstige is one of the most attractive ranges for new entrants. It supports better fragrance, stronger packaging, and more refined claim architecture without forcing ultra-premium expectations too early.

Premium tier products require stronger formula experience, stronger branding, and either clinical framing or highly polished salon-style delivery.

For many private label and OEM launches, masstige is the most commercially balanced entry point.

Price Segmentation: Entry to Premium Tier

Product Format and Size Strategy

Liquid shampoo remains the core format and should still be the default starting point for most new brands. It is the most scalable, the most channel-flexible, and the easiest to merchandise.

Treatment shampoos offer the strongest margin potential because they move the category away from pure commodity cleansing and toward outcome-oriented care.

Specialty shampoos such as color-safe, clarifying, hard-water defense, curl hydration, frizz-control, and thickening are often the best route for later SKU expansion once the hero product proves traction.

In terms of size, 300–500 mL remains the most practical range for mainstream and premium retail. Travel sizes can be strategically useful for Amazon bundles, trial, salon sampling, and premium conversion.

Competitive Landscape

The U.S. shampoo market in 2026 is organized around several leading positioning clusters.

Functional problem-solution products focus on dandruff, buildup, oily scalp, thinning appearance, itch, and clarifying needs. These perform especially well in search-driven channels.

Clean and lifestyle-coded shampoos still have a place, but this space is crowded. Products need a sharper performance promise to stand out.

Salon and professional-inspired shampoos focus on bond repair, gloss, strength, frizz smoothing, and color maintenance. These territories remain attractive for masstige and premium pricing.

Scalp-led and dermatology-coded shampoos benefit from higher trust and stronger repeat purchase, but they also require more regulatory discipline.

The most crowded spaces include generic sulfate-free shampoos, broad “natural shampoo for all hair types” positioning, and me-too bond-repair products without credible differentiation.

The most interesting gaps include premium-accessible scalp balance, clarifying shampoos that preserve moisture, better textured-hair cleansing systems, sensitive-scalp comfort products, and Amazon-optimized hero shampoo plus bundle strategies.

Recommended SKU Architecture

A more effective shampoo line should not begin with too many disconnected SKUs. It should begin with a structured product system.

A strong starter architecture usually includes:

- one hero SKU that drives traffic

- one conversion SKU with more targeted use-case relevance

- one premium SKU that expands margin

- one bundle strategy that supports higher AOV and stronger retention

A hero SKU is usually best built around scalp balance or bond repair because these offer broad audience fit and strong search behavior.

A conversion SKU should solve a more specific problem, such as clarifying without stripping or moisture retention for textured hair.

A premium SKU should feel more elevated in formula, sensory delivery, and package presentation, such as bond-repair premium or color-protect gloss.

Bundle logic should vary by channel, but shampoo plus conditioner remains the most dependable starting point.

Best-Selling SKU Patterns & Key Differentiators

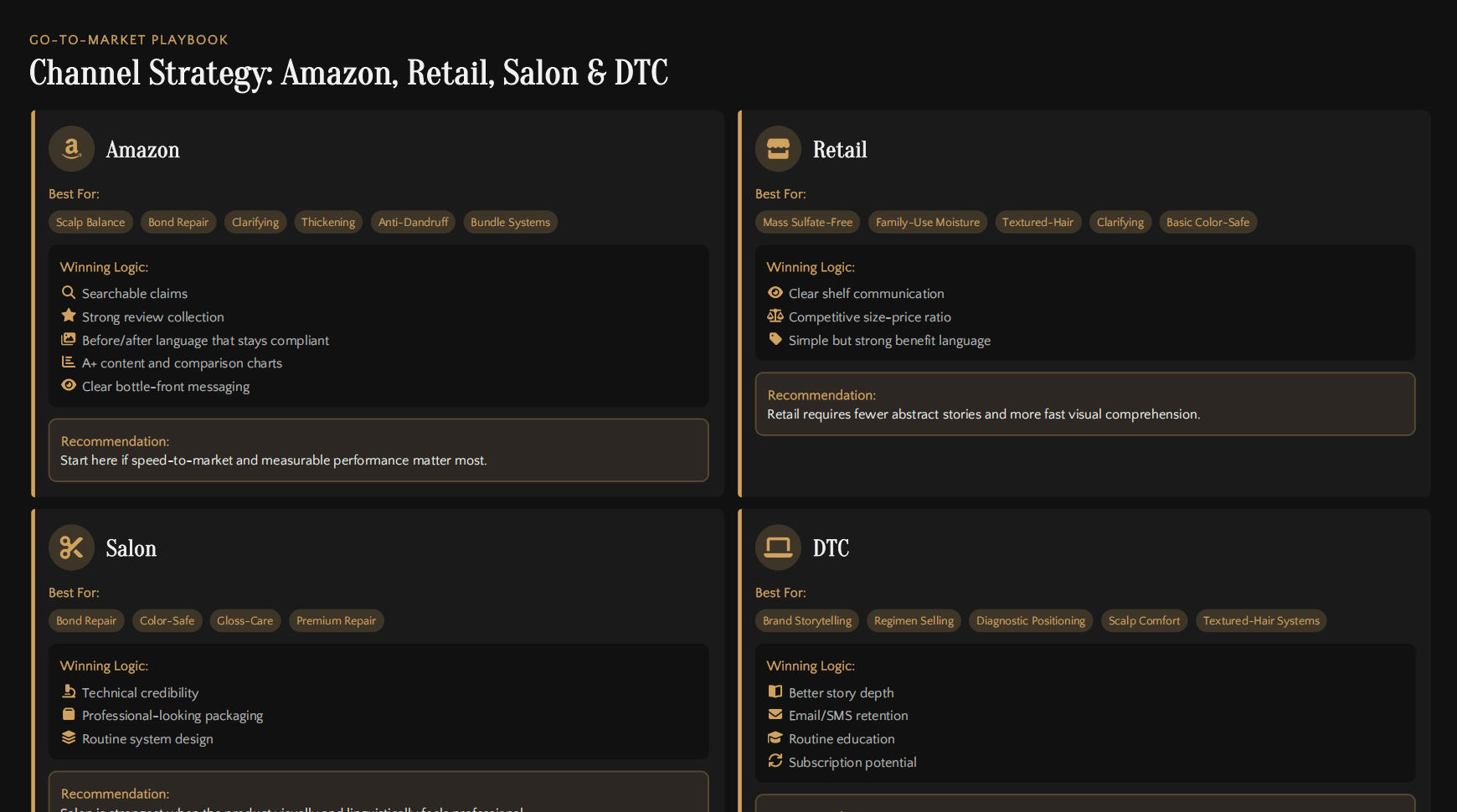

Channel Strategy

The strongest shampoo launch should be channel-aware from day one.

Amazon is especially effective for scalp balance, bond repair, clarifying, thickening, anti-dandruff, and bundle systems. It rewards searchable claims, review growth, A+ content, and immediate bottle-front clarity.

Retail works best for broad but clear need states such as moisturizing, color-safe, textured-hair, clarifying, and family-use shampoos. Shelf comprehension matters more than abstract storytelling.

Salon is best for repair, gloss, color-safe, and premium system-oriented shampoos. Professional language and packaging credibility are important.

DTC works especially well for regimen selling, scalp-comfort education, textured-hair systems, and higher-story categories where email retention and content depth support repeat purchase.

The best strategy is rarely one-channel-only. It is usually a channel-prioritized launch with packaging and messaging adapted to where the product sells first.

Channel Strategy: Amazon, Retail, Salon & DTC

Compliance and Risk Control

One of the biggest operational risks in shampoo is claim drift. Brands often start with a cosmetic formula but move too far into drug-type language, especially around dandruff, hair loss, scalp treatment, or regrowth.

That distinction matters. Cosmetic shampoos cleanse, improve feel, softness, shine, and appearance. OTC-functional shampoos require a different regulatory and labeling pathway.

Other common risks include:

- entering overcrowded spaces with weak differentiation

- using premium pricing without premium formula payoff

- creating harsh clarifying products that damage repeat purchase

- overloading formulas with fragrance or essential oils in scalp-sensitive segments

- delaying packaging compatibility checks until too late

The more functional the promise, the more disciplined the development process needs to be.

OEM Launch Strategy

The fastest way to improve OEM execution is to provide a sharper brief from the start.

A stronger buyer brief should include:

- target consumer

- core problem to solve

- price band

- benchmark products

- packaging preferences

- target channel

- claims boundary

- formula philosophy

- fragrance direction

- size plan

- testing requirements

- launch timeline

A shampoo project moves much faster when the buyer does not say “make me a shampoo,” but instead says “make me a scalp balance daily shampoo for oily roots and buildup at this price for this channel.”

That level of clarity reduces wasted samples, improves quoting, and helps both brand and manufacturer align earlier around performance, packaging, and commercialization logic.

What to Launch First

For most new entrants, the best first launch is a sulfate-free scalp and damage balance shampoo in the masstige tier.

This is the most commercially efficient entry point because it sits at the intersection of frequent purchase, broad audience fit, Amazon friendliness, and premium-enough positioning.

The ideal first SKU should:

- cleanse effectively

- support scalp comfort

- reduce stripped feel

- speak to buildup and daily stress

- remain compatible with broader damage or color-stress positioning

- leave room for future line extension into conditioner, scalp serum, repair mask, or travel-size bundle

This creates a stronger starting platform than a generic sulfate-free shampoo or an overly narrow first SKU.

Final Takeaway

The U.S. shampoo market in 2026 is still large, but it is no longer a category that rewards generic cleansing products. Growth is concentrating around more targeted need states, stronger sensory expectations, clearer claim architecture, and more channel-aware product systems.

The brands most likely to win are not the ones launching the most SKUs. They are the ones building the clearest product logic: one defined problem, one strong benefit promise, one channel-fit format, and one formula experience that earns repeat purchase.

If your team is evaluating a shampoo launch for the U.S. market, the strongest next step is to align need state, claims boundary, price band, channel strategy, and OEM brief first, then move into sampling with a much clearer commercial objective.

Download the Full Report (PDF)

Tell us your target region, product category, and the decision you’re trying to make. We’ll suggest the closest existing report—or build a tailored version.