Executive Summary

This report explores the U.S. hair mask market in 2026, including consumer demand, product positioning, price structure, packaging strategy, channel fit, compliance priorities, and OEM launch planning. It is designed to help brands, distributors, Amazon sellers, and product development teams turn category insight into a more practical treatment-led launch strategy.

U.S. Hair Mask Market Report 2026: Consumer Trends, Pricing, Channel Strategy, and OEM Launch Guide

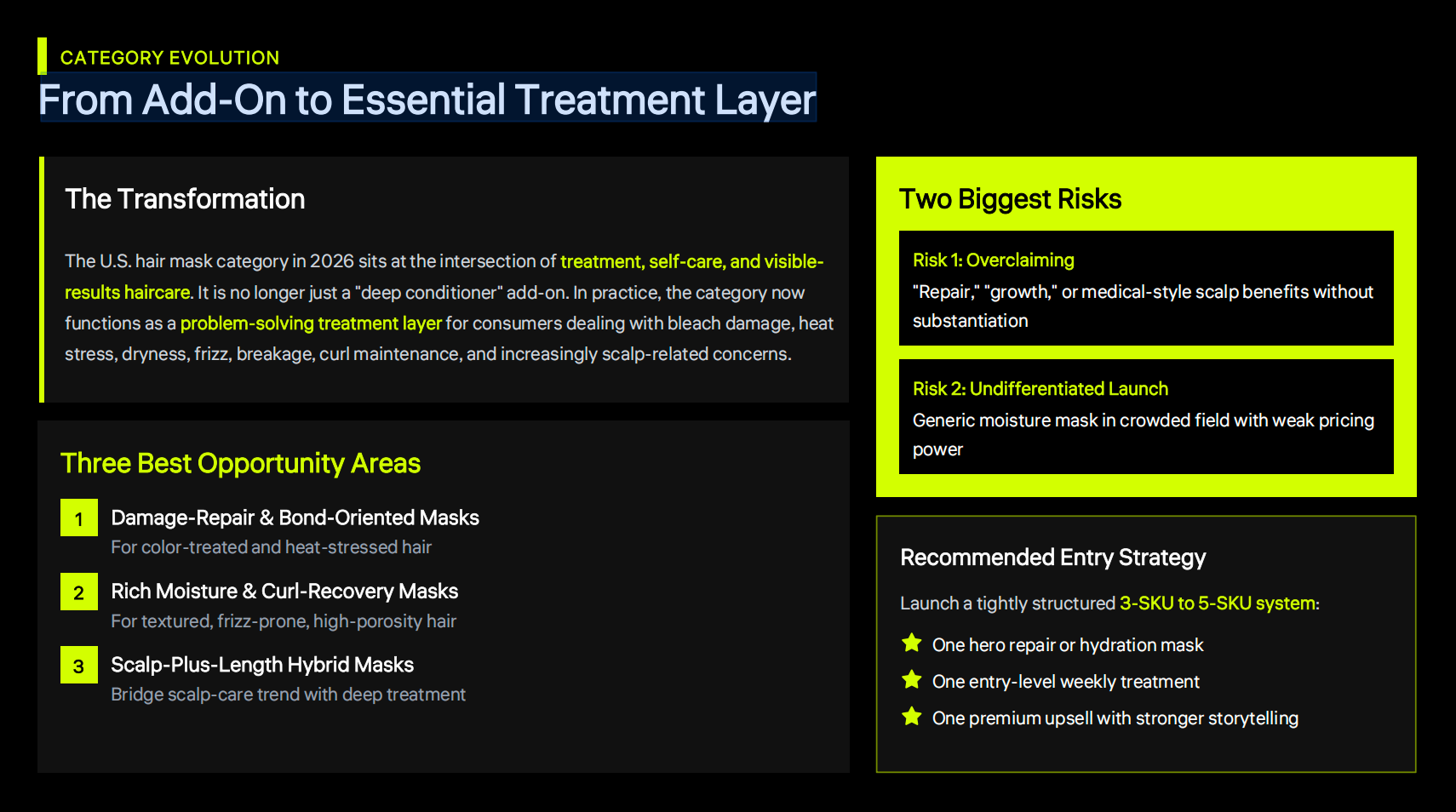

The U.S. hair mask market in 2026 is no longer just an extension of deep conditioner. It has become a treatment-led category shaped by visible-results haircare, self-care rituals, targeted problem solving, and premiumization.

Consumers are no longer looking for generic moisture alone. They are increasingly choosing hair masks based on a clear use case: damage recovery after bleaching, weekly hydration for dry or frizz-prone hair, curl recovery after wash day, heat-stress repair, or scalp-plus-length treatment.

For brands, importers, distributors, and e-commerce sellers, this means the category should be approached as a treatment business rather than a routine conditioner business. The most commercially promising launches are built around a disciplined product system, clear channel fit, and a stronger connection between formula, packaging, pricing, and consumer problem.

This report translates category demand into a practical launch roadmap. It covers consumer signals, product positioning, price structure, packaging strategy, channel logic, compliance priorities, and OEM execution planning for brands entering or expanding in the U.S. hair mask market.

Executive Summary

The U.S. hair mask category is moving toward treatment-led premiumization. Consumers are spending more intentionally inside haircare, especially when a product promises visible improvements such as smoother feel, less roughness, reduced breakage appearance, softer ends, easier detangling, and improved shine.

In practical terms, hair masks now function as the reset or repair step inside a broader routine. They sit between everyday conditioner and more specialized styling or finishing products. Conditioner remains maintenance. Hair oil is often seen as finish and shine. Leave-ins solve convenience and styling. Hair masks are where consumers go when they want to fix, restore, recover, or deeply treat.

For most new entrants, the strongest 2026 opportunity is not a broad generic moisture mask. It is a focused system built around one hero treatment territory, one easier entry SKU, and one premium upsell. This creates better pricing power, clearer content strategy, and a faster path to repeat purchase.

Market Opportunity Overview

The market is being shaped by three major shifts.

The first is treatment behavior. Consumers are increasingly buying haircare in a more problem-solution way. Instead of asking for “something nourishing,” they are asking for products that support damaged hair, frizz control, curl recovery, scalp comfort, or post-bleach softness.

The second is premiumization. Hair masks are benefiting from the same logic that lifted bond-building systems, prestige treatments, and scalp-care products. Buyers are willing to pay more when the use occasion is specific and the result feels measurable.

The third is routine integration. Hair masks are increasingly bought as part of a larger system that includes cleansing, treating, protecting, and finishing. That gives the category stronger bundling logic, higher AOV potential, and better repeat behavior.

For a new brand, the practical conclusion is simple: do not position hair masks as generic conditioner extensions. Position them as high-margin treatment SKUs with a sharper problem-solution story.

What Is Driving Demand in 2026

The category is growing because consumers increasingly associate hair masks with visible recovery, not just softness.

The most commercially relevant demand scenarios include:

- post-color or post-bleach repair

- weekly hydration for dry, dull, or frizz-prone hair

- curl and coil recovery after wash day

- heat-stress recovery for frequent hot-tool users

- scalp comfort and reset

- event-prep or travel use for quick improvement

This is why masks perform best when they clearly own one treatment territory such as repair, hydration, strength, or scalp-plus-length renewal.

Products that try to solve every hair problem at once often lose clarity in both retail and digital channels. The stronger move is to choose one primary usage occasion and one secondary usage occasion, then build the product around that logic.

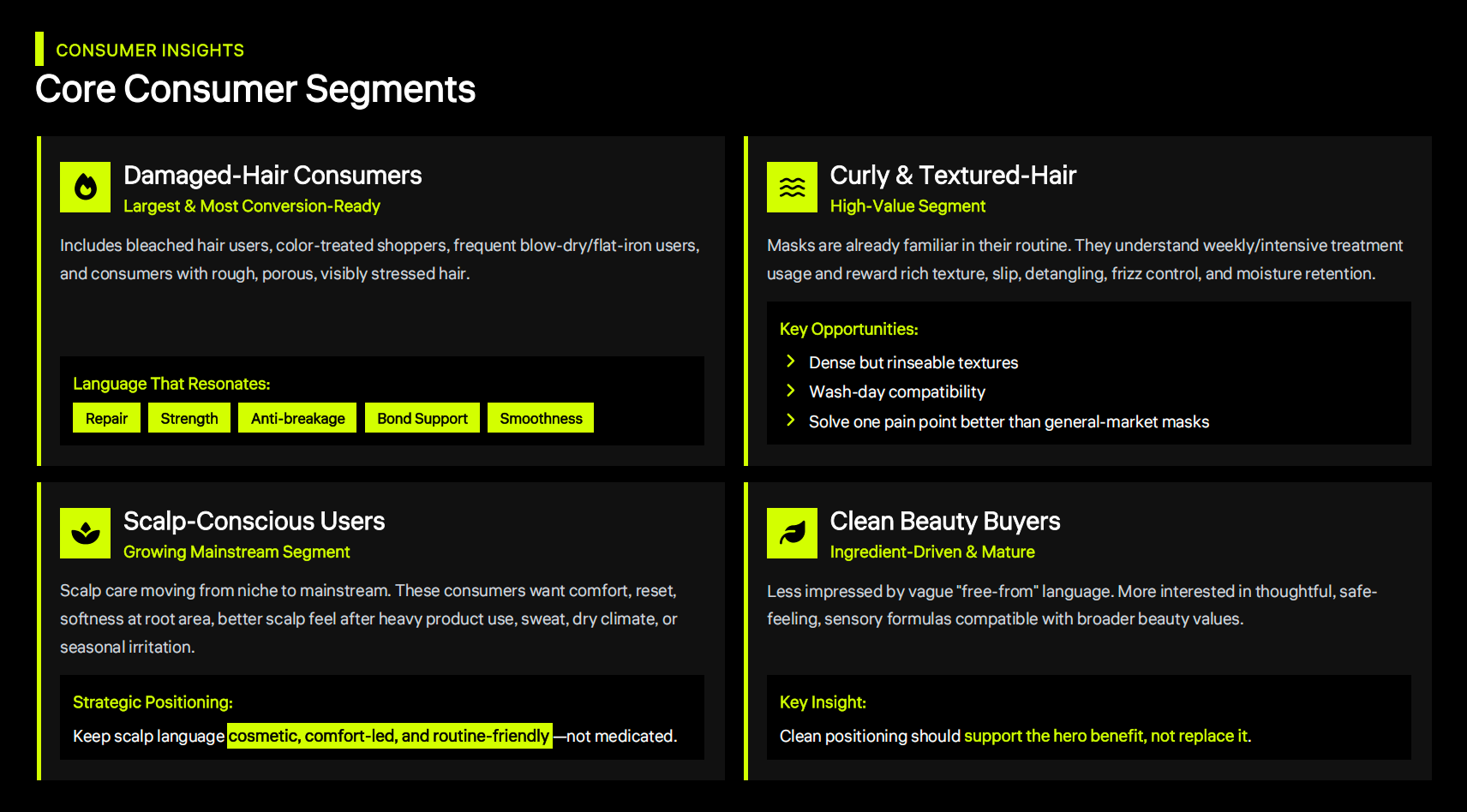

Core Consumer Segments

The damaged-hair consumer remains the broadest and most conversion-ready segment. This includes color-treated users, bleached-hair users, frequent hot-tool users, and consumers dealing with visible roughness, porosity, or breakage. This group responds well to language around repair, strength, anti-breakage, smoothness, and recovery.

Curly and textured-hair consumers are another high-value segment because masks are already a familiar part of their routine. They tend to care more about slip, detangling, softness, frizz control, wash-day compatibility, and moisture retention.

Scalp-conscious consumers are becoming more important as scalp care moves into the mainstream. Many of these buyers are not looking for a medical solution. They want comfort, freshness, reset, and a better-feeling scalp without losing softness through the hair lengths.

Ingredient-aware consumers still matter, but clean positioning alone is no longer enough. They still value vegan direction, silicone-free architecture, recyclable packaging, and ingredient transparency, but performance storytelling now matters more than values language alone.

The takeaway is clear: benefit comes first, clean support comes second.

Core Consumer Segments

Product Positioning: Where the Best Opportunities Are

In 2026, the strongest launch lanes are not generic “for all hair types” masks. The best opportunities are more clearly defined.

The most promising positioning territories include:

- bond repair for color-treated and heat-damaged hair

- deep hydration for dry, frizz-prone, and high-porosity hair

- curl-recovery masks for textured hair

- fine-hair-safe repair masks that do not feel heavy

- scalp-plus-length hybrid masks with cosmetic comfort positioning

- post-bleach recovery masks with a soft premium voice

- event-ready shine masks for quick softness and polish

A new brand does not need to cover all of these at launch. It needs to choose the one territory that gives the clearest shelf identity and the most believable price logic.

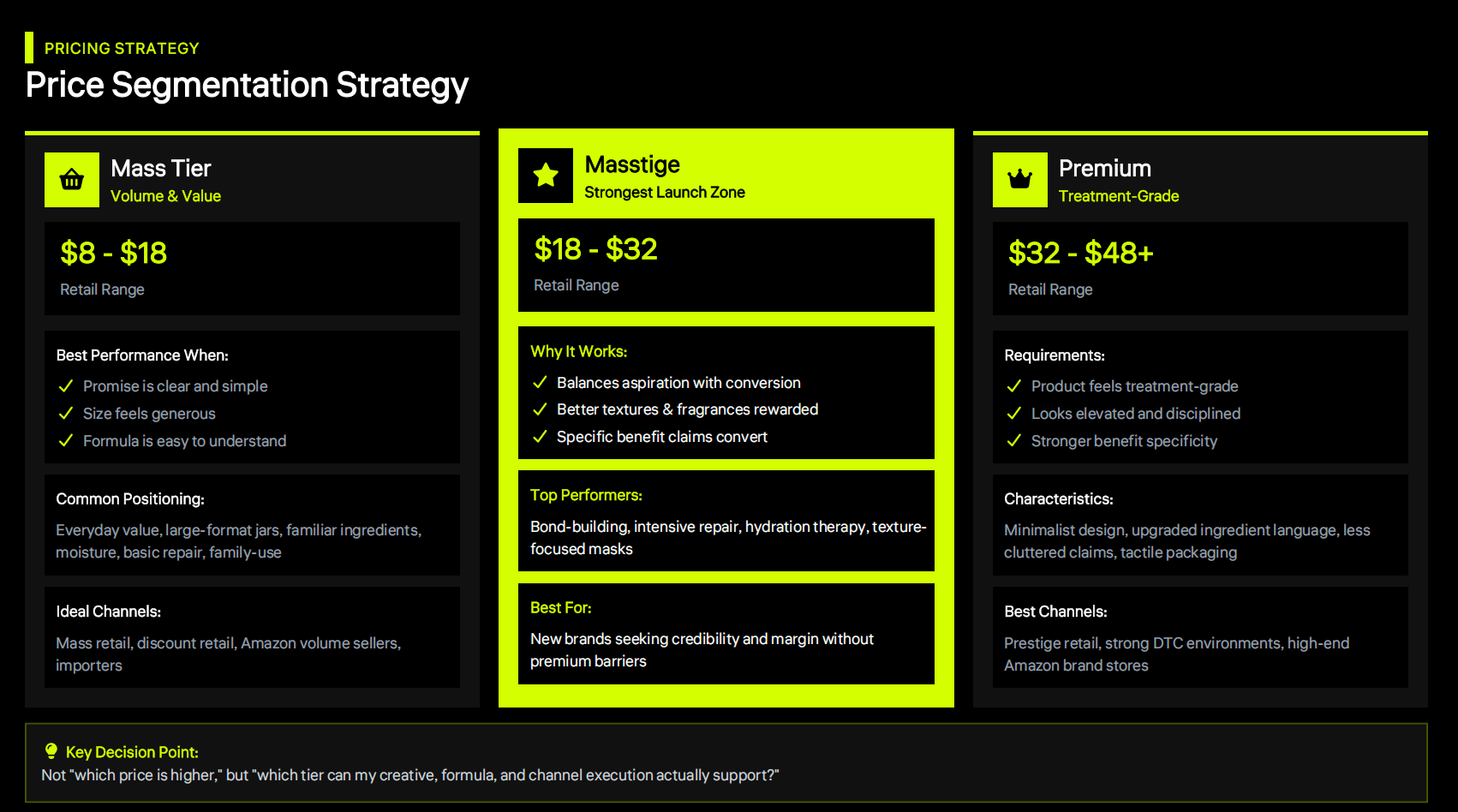

Price Tier Strategy

The category is clearly segmented into mass, masstige, and premium.

Mass products perform best when the promise is easy to understand, the size feels generous, and the formula story is familiar. This is where large-format jars and straightforward moisture or repair messages tend to work.

Masstige is often the strongest launch zone for new brands because it balances aspiration with conversion. Consumers here are willing to pay more for better textures, better fragrance, stronger packaging, and more specific benefit stories.

Premium works when the product feels treatment-grade, visually disciplined, and more technically positioned. This tier benefits from more focused claims, upgraded packaging, and less visual clutter.

For most OEM clients, the key question is not which tier sounds more impressive. It is which tier the formula, packaging, and channel strategy can genuinely support.

Price Segmentation Strategy

Format and Packaging Strategy

Jars remain the dominant format because they communicate richness, ritual, and value. They work especially well for thick textures, textured-hair positioning, and spa-like self-care use.

Tubes are strategically stronger than many brands assume. They feel cleaner, more modern, more travel-friendly, and often work better for Amazon, DTC, and treatment-first visual positioning.

Sachets and mini sizes are not the hero format, but they are very useful for trial, sampling, bundles, salon adjacencies, and lower-risk entry into more premium treatment lines.

Format should not be chosen only for manufacturing convenience. It should be chosen as part of positioning.

A simple rule:

- use jars when ritual and richness are core to the offer

- use tubes when convenience and treatment credibility matter more

- use sachets or minis to reduce trial friction and support bundling

Claims Strategy and Product Story

“Repair” remains the most broadly usable claim territory because consumers understand it quickly. But it is also crowded, so the strongest repair positioning usually sharpens the context: repair for bleached hair, repair for brittle ends, repair for heat damage, or repair for fine fragile hair.

“Bond-building” is more premium and technical. It suggests science, seriousness, and stronger treatment logic, but it also raises expectations. It works best when the overall formula and packaging story support that level of credibility.

“Deep hydration” remains one of the safest and most repeatable launch lanes, especially for dry hair, textured hair, winter use, and frizz-prone consumers.

“Scalp + hair hybrid” is still underdeveloped enough to matter, especially in DTC and selective prestige channels. It offers a more original narrative, as long as the language remains cosmetic and comfort-led rather than medical.

The strongest product story usually includes one primary promise and one support promise. Too many front-label claims weaken trust.

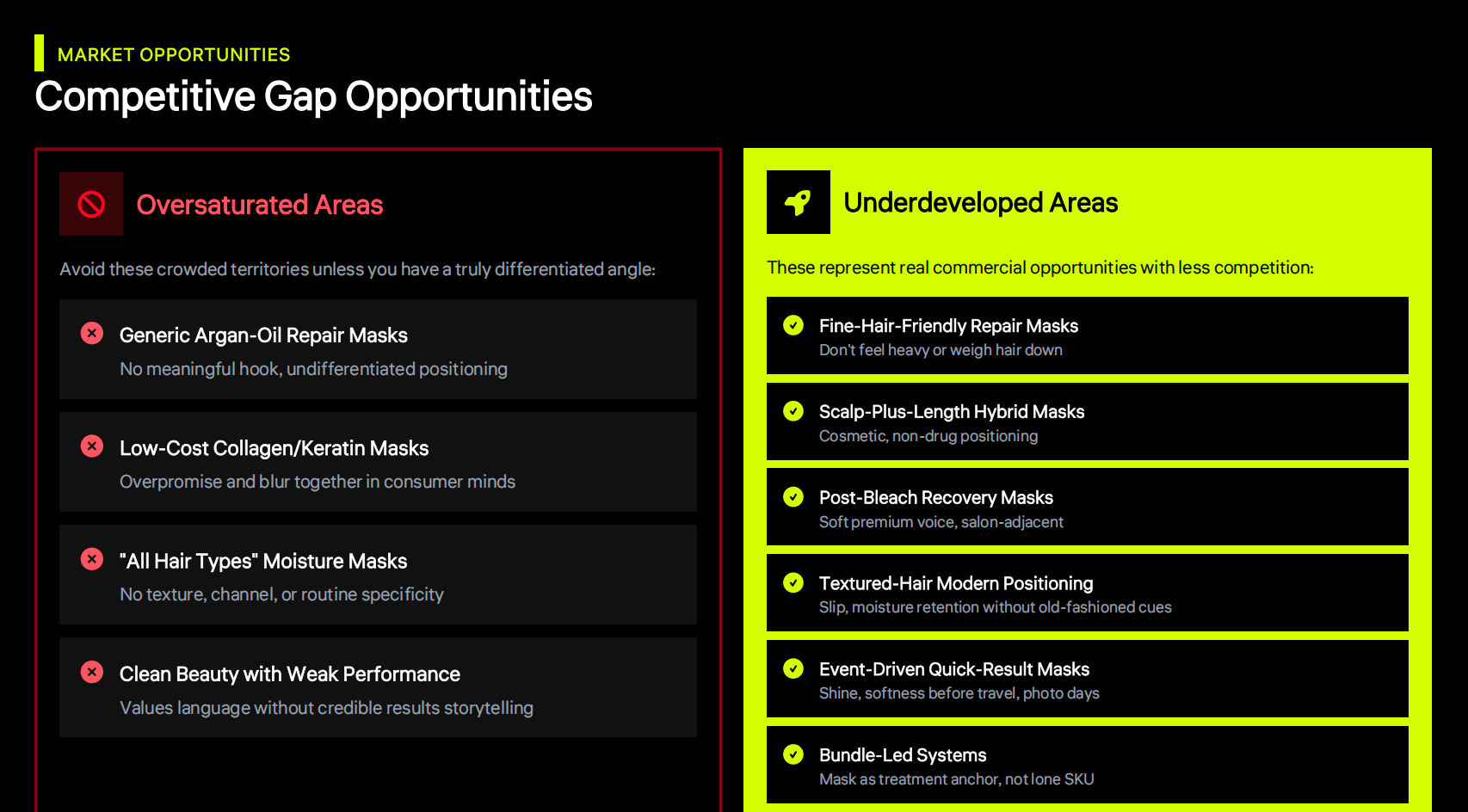

Competitive White Space

The current market is crowded, but not closed.

Oversaturated areas include:

- generic argan-oil repair masks without a clear hook

- low-cost keratin or collagen masks that overpromise

- “all hair types” moisture masks with weak differentiation

- clean beauty masks that emphasize values but not outcomes

Underdeveloped areas include:

- fine-hair-friendly repair masks

- scalp-plus-length hybrid masks

- post-bleach recovery masks with premium positioning

- textured-hair masks with stronger modern packaging

- event-driven shine or softening masks

- system-led mask launches where the mask anchors a broader routine

This is where new entrants have room to win: not by copying the biggest prestige brands, but by owning a sharper use case and a more commercial SKU structure.

Competitive Gap Opportunitiesœ

Recommended Launch Logic

The strongest first launch is usually not ten SKUs. It is a focused system.

A practical first structure often includes:

- one hero SKU with the strongest treatment story

- one broader entry SKU with easier repeat logic

- one upsell SKU with stronger ritual or premium positioning

- one mini or sachet extension for trial

- one specialty SKU only if it clearly serves a distinct audience

Good launch combinations include:

- hero bond repair + entry hydration + overnight premium upsell

- hero deep hydration + rosemary strength entry + fine-hair repair specialty

- hero curl recovery + sachet trial + scalp-plus-length innovation hook

This structure makes marketing more coherent, improves bundle design, and reduces SKU overlap.

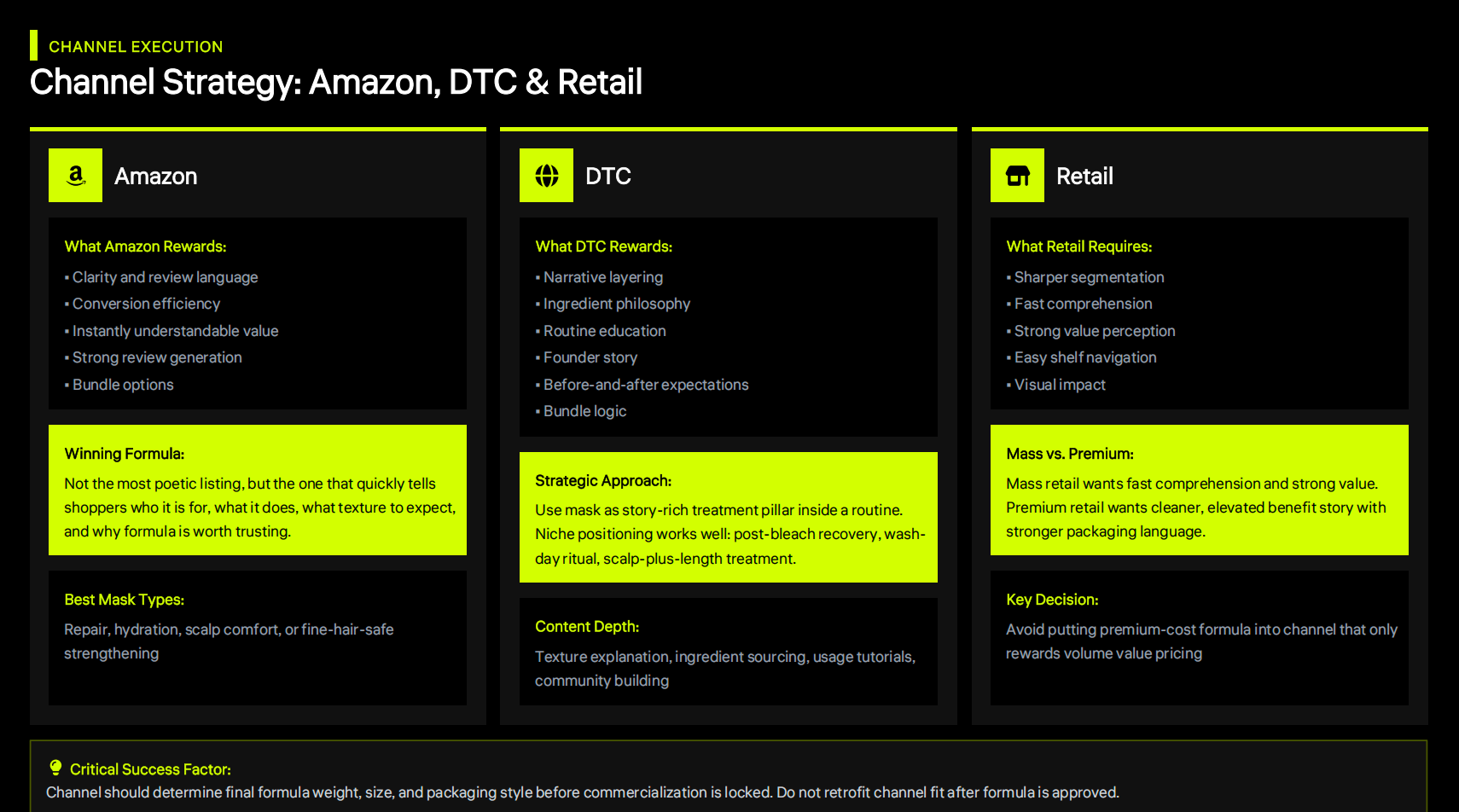

Channel Strategy

A hair mask launch should be channel-specific from the beginning.

For Amazon, success depends on clarity, review language, easy benefit recognition, and conversion efficiency. The product needs to quickly tell shoppers who it is for, what problem it solves, what texture to expect, and why the result is believable.

For DTC, the mask should function as the treatment pillar inside a broader routine. This is where ingredient philosophy, texture explanation, routine education, bundles, and founder or brand narrative matter more.

For retail, positioning must become even sharper. Mass retail wants fast value comprehension and easy shelf navigation. Premium retail wants cleaner visual hierarchy, stronger benefit discipline, and better packaging language.

The key rule is this: channel should determine formula weight, size, packaging style, and final claim structure before commercialization is locked.

Channel Strategy: Amazon, DTC & Retail

Compliance and Quality Considerations

Hair masks are cosmetic products, and the wording needs to stay within that framework.

The safest and most scalable language focuses on:

- appearance

- softness

- manageability

- visible dryness

- smoother feel

- less roughness

- detangling

- shine

- comfort

Brands should be careful with claims that suggest drug-style scalp treatment, guaranteed hair growth, permanent structural repair, or exaggerated “clean” promises that cannot be supported.

Stability, preservation robustness, packaging compatibility, and formula consistency are all commercially critical in this category. A good concept can still fail if the texture changes over time, the fragrance shifts, or the packaging performs badly in repeated bathroom use.

A strong launch should treat compliance and quality as part of product strategy, not as administrative cleanup after development.

OEM Execution Plan

For OEM and private label launches, the strongest results come from a clearer brief.

A useful RFQ should define:

- target market and channel

- target consumer and main hair concern

- lead benefit territory

- target retail price

- reference benchmarks

- preferred size and packaging style

- expected launch timing

- first-order quantity

- compliance sensitivity level

- whether the project is Amazon-first, DTC-first, or distributor-led

For many first launches, the best execution model is semi-custom: a customized formula and artwork using proven packaging components. This reduces MOQ pressure, shortens lead times, and keeps the project more commercially realistic.

Over-customization too early is one of the easiest ways to slow speed and weaken channel fit.

What Brands Should Do Next

If you are entering the U.S. hair mask market, the next step is not simply choosing a formula base.

The better sequence is:

- define one primary consumer problem

- choose one lead treatment territory

- confirm your launch channel

- align texture and packaging with the target consumer

- set a realistic price tier

- decide whether the mask is standalone or part of a system

- prepare your RFQ with commercial clarity before sampling starts

That sequence reduces wasted rounds, improves costing, and leads to a much more usable launch assortment.

Final Takeaway

The U.S. hair mask market in 2026 is attractive because it sits at the intersection of treatment, self-care, premiumization, and routine-based repeat purchase.

The brands most likely to win are not the ones with the broadest “moisture for all” message. They are the ones with the clearest treatment logic, the sharpest channel fit, the best SKU separation, and the strongest balance between formula credibility and marketability.

If your team is evaluating a new hair mask launch, the smartest move is to define the problem, channel, price tier, and SKU structure first, then move into sampling with a much clearer commercial brief.

Download the Full Report (PDF)

Tell us your target region, product category, and the decision you’re trying to make. We’ll suggest the closest existing report—or build a tailored version.