Executive Summary

This report explores the U.S. hair growth market in 2026, including consumer demand, thinning-related product opportunities, scalp-support positioning, format strategy, channel fit, compliance priorities, and OEM launch planning. It is designed to help brands, distributors, sourcing teams, and e-commerce sellers turn market insight into a more practical product launch strategy.

U.S. Hair Growth Market Report 2026: Consumer Trends, Product Formats, and OEM Launch Strategy

The U.S. hair growth market in 2026 should not be treated as a standard beauty category. It is a treatment-minded, trust-sensitive, and claim-constrained market shaped by visible thinning, stress-related shedding, postpartum recovery, aging, and male pattern hair loss.

For brands, distributors, sourcing teams, and e-commerce sellers, the real opportunity is not in launching another generic hair serum. The stronger path is to build a focused, problem-led product architecture that fits real consumer concerns, realistic usage timelines, compliant positioning, and channel-specific economics.

This report translates the category into launch logic. It covers consumer demand, product formats, pricing, packaging, channel strategy, compliance priorities, and OEM opportunities for businesses entering or expanding in the U.S. hair growth market.

Executive Summary

The U.S. hair growth market is becoming increasingly mainstream, but it is also becoming more demanding. Consumers are not shopping for simple beauty enhancement alone. They are shopping for visible progress, stronger routine logic, better scalp support, and clearer proof over time.

This changes how products should be developed and marketed. In this category, packaging design, claims language, texture, routine compliance, and product format all matter as much as ingredient stories. Consumers want products that feel believable, easy to use, and worth continuing for at least 8 to 12 weeks.

For most new entrants, the strongest route in 2026 is not a large collection. It is a tighter assortment built around one trust anchor, one support SKU, and one repeat-use retention format. That means launching with a hero scalp serum or tonic, supported by a secondary scalp care product and a regimen story designed for 90-day use rather than impulse purchase alone.

Market Opportunity Overview

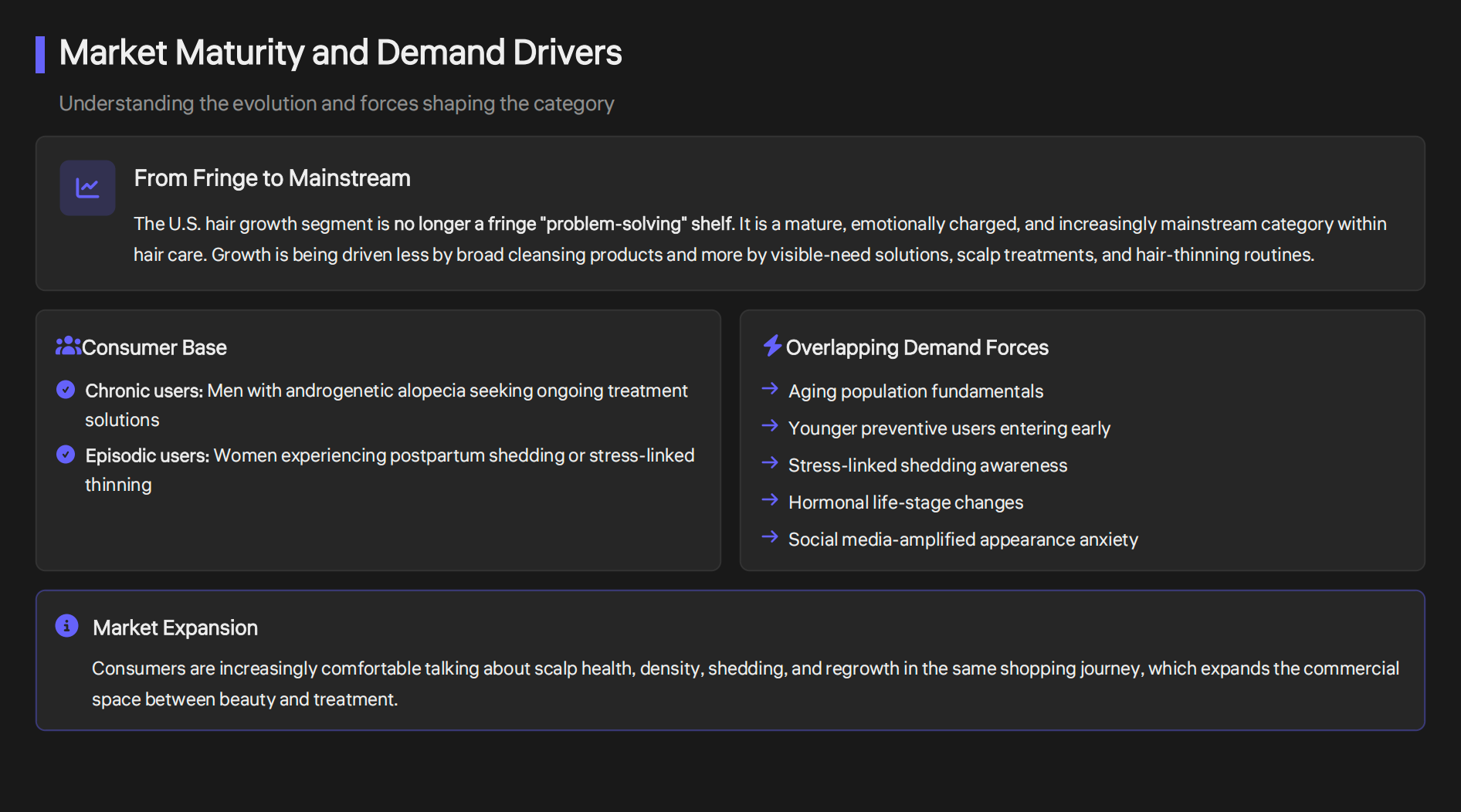

The U.S. hair growth segment is no longer a niche problem-solving shelf. It has become a larger, more emotionally visible category supported by both chronic users and episodic users.

Some consumers enter the market because of male pattern hair loss. Others are driven by postpartum shedding, stress-linked thinning, widening part lines, breakage, or early preventive concerns. These multiple entry points make the category commercially attractive, but they also make it more complex. One product and one message cannot serve every user equally well.

The strongest opportunity in 2026 is not broad beauty positioning. It is problem-specific positioning with realistic outcomes, a clear usage period, and a product system that supports repeat use.

Market Maturity and Demand Drivers

What Is Driving Demand

Several forces are shaping the market.

The first is visible need. Consumers often shop after noticing clear changes such as increased shedding, weaker hairlines, reduced density, or scalp discomfort.

The second is treatment mindset. Buyers increasingly expect products to support visible improvement over time, not just make hair feel softer or shinier.

The third is trust. Hair growth is a high-anxiety category, which means consumers respond better to disciplined claims, clear use instructions, and believable timeframes than to exaggerated promises.

The fourth is routine design. Products that feel too greasy, inconvenient, or unclear in their role are more likely to be abandoned, even if the concept sounds attractive at first.

This means the market rewards products that are easier to trust, easier to use, and easier to repurchase.

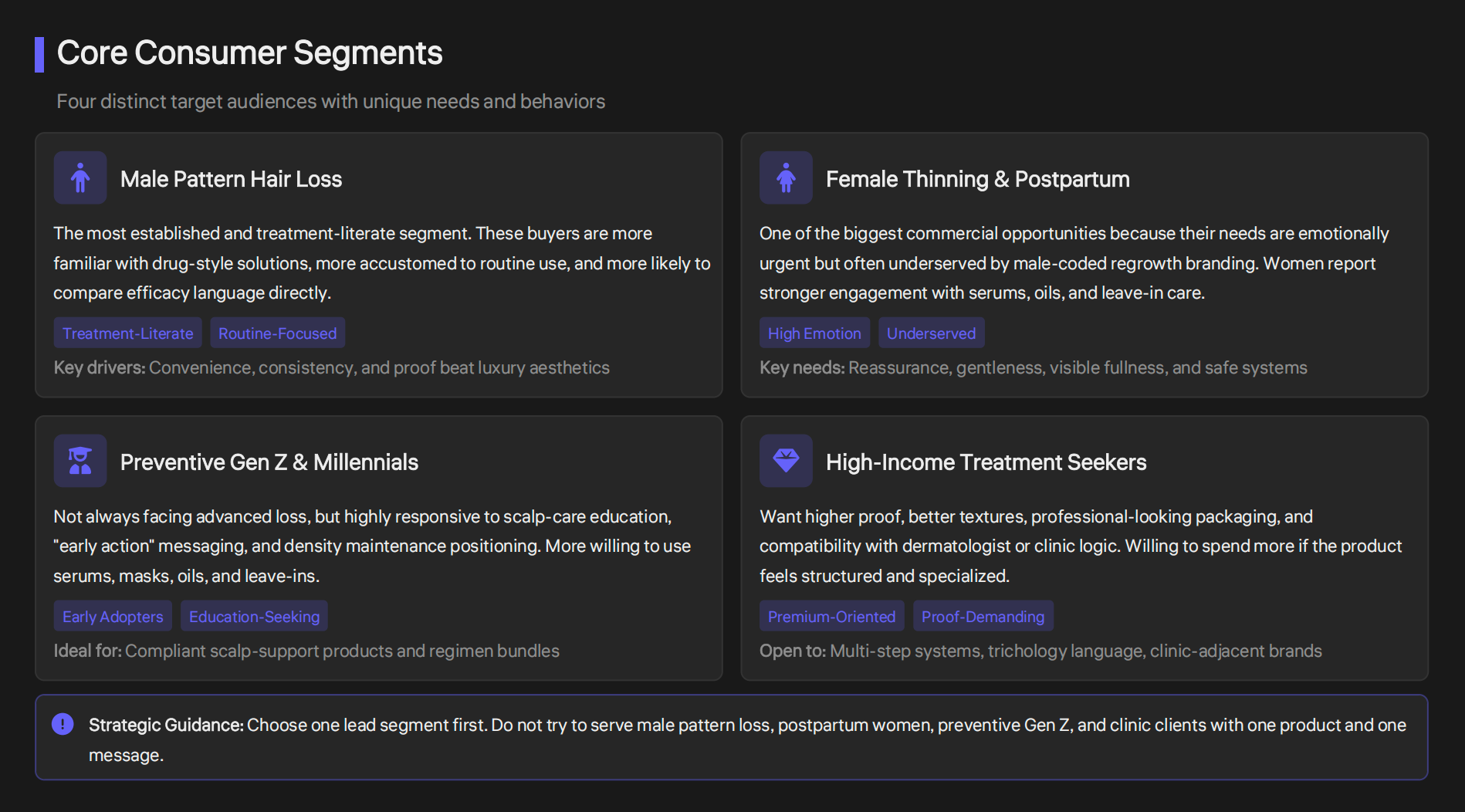

Core Consumer Segments

A practical launch in the U.S. hair growth market should begin with one clearly defined lead segment.

The most commercially relevant segments include:

- men with early recession or diffuse thinning

- women with mild to moderate thinning

- postpartum users looking for scalp and density support

- preventive Gen Z and Millennial users

- premium treatment seekers who prefer clinic-inspired systems

- textured-hair users who respond better to scalp nourishment and breakage-reduction logic

Each of these groups enters the category for different reasons. Men often prioritize simplicity and daily compliance. Postpartum users want reassurance, gentleness, and lower-risk support language. Preventive consumers want early action and scalp wellness. Premium treatment seekers expect stronger proof and more structured routines.

That is why product briefs should begin with one lead user, not with a vague “for all hair growth needs” concept.

Core Consumer Segments

Product Formats with the Strongest Commercial Potential

In 2026, the U.S. hair growth market is increasingly format-driven. Consumers do not only buy by ingredient story. They buy by how the product fits daily use.

The strongest product formats include:

- scalp density serums

- fast-dry scalp tonics

- scalp-support oils

- leave-in density treatments

- pre-treatment scalp exfoliation products

- 90-day system kits

- drug-adjacent comfort products for users already following a more intensive regimen

Among these, serum and tonic formats remain the strongest hero-product candidates because they communicate treatment logic, fit Amazon and DTC well, and are easiest to integrate into a daily habit.

Oils work best when the audience already accepts scalp oiling behavior or values nourishment and breakage support. Leave-in treatments are especially useful when the brand wants to combine immediate cosmetic payoff with longer-term retention logic.

Best First Product Strategy

Most brands should not enter this category with ten SKUs. A stronger first launch usually includes:

- one hero scalp serum or tonic

- one support SKU

- one retention or routine-expanding SKU

A practical example would be:

- a daily scalp density serum as the hero

- a postpartum recovery tonic or scalp oil as support

- a density leave-in or 90-day regimen kit as the retention layer

This structure works because it balances clarity with enough depth to improve repeat purchase and average order value. It also reduces working-capital pressure and makes customer feedback easier to interpret in the early stage.

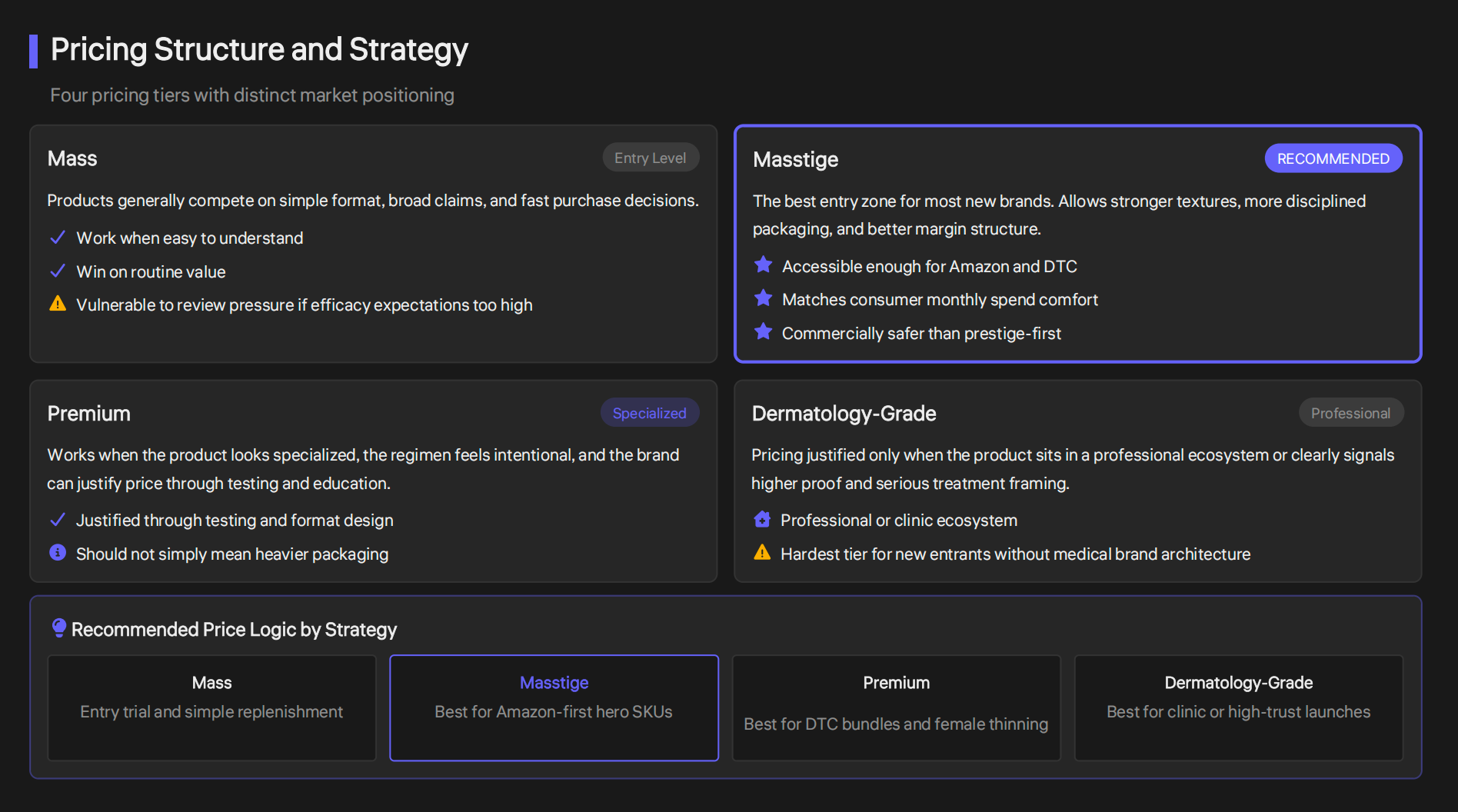

Pricing Strategy

The U.S. hair growth market can be divided into mass, masstige, premium, and clinic-adjacent pricing, but not every tier is equally suitable for a new entrant.

Mass is useful for trial and fast access, but it is highly exposed to review pressure and price sensitivity. Premium can work, but only when the product looks specialized and is supported by stronger education and proof architecture. Clinic-adjacent positioning is even harder unless the brand already has medical, professional, or highly clinical credibility.

For most new brands, masstige is the most commercially practical entry point. It allows:

- better textures

- stronger packaging discipline

- healthier margin structure

- enough accessibility for Amazon and DTC buyers

- more believable repeat-use economics

That is why the safest launch path for many new operators is masstige hero SKU first, premium system second.

Pricing Structure and Strategy

Packaging Strategy

Packaging in the hair growth category should communicate seriousness, not fantasy.

Consumers in this segment generally trust restrained, treatment-like packaging more than decorative or overly beauty-coded presentation. The visual system should reinforce product discipline, routine use, and confidence.

Useful packaging directions include:

- spray formats for speed and compliance

- dropper formats for premium precision

- narrow-nozzle or clinical-pack cues for focused scalp use

- low-residue, low-mess application systems

- clean typography and structured hierarchy

- packaging that clearly signals daily use and visible progress over time

For this category, packaging is not just about appearance. It directly affects whether the user will keep using the product consistently.

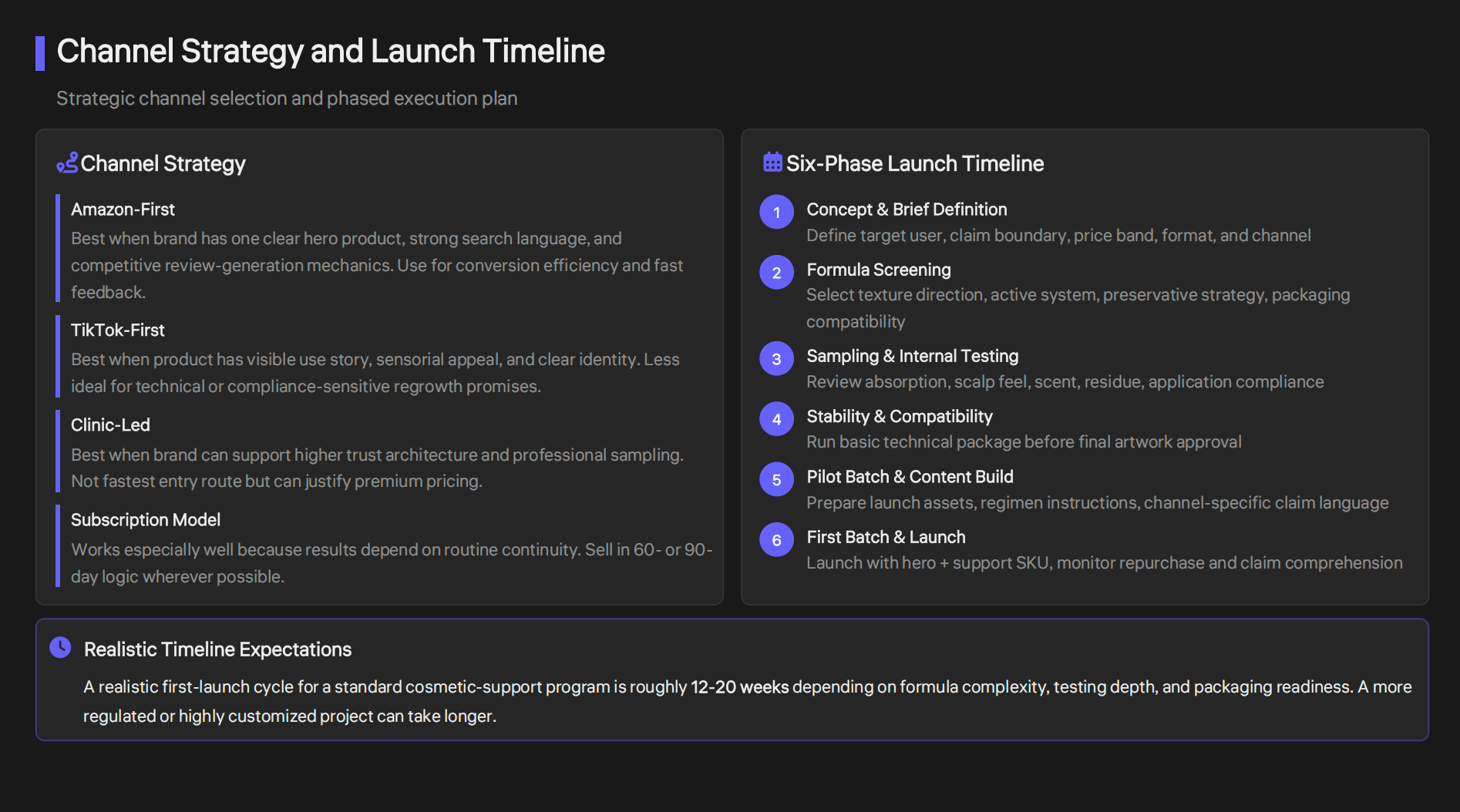

Channel Strategy

A strong U.S. hair growth launch should be built for channel fit from the beginning.

For Amazon, the best route is usually one hero SKU with clear functional positioning, strong search alignment, and repeat-use logic. The platform rewards products that are easy to understand, easy to review, and easy to repurchase.

For DTC, the opportunity is broader. The brand can explain regimen logic, educate different user groups, collect customer data, and sell 60- or 90-day systems more effectively.

For TikTok-driven selling, products need a visible usage story, such as postpartum recovery, scalp ritual, or baby-hair journey. Texture, demonstration, and immediate narrative clarity matter much more here.

For clinic or professional channels, the product needs stronger trust architecture, more disciplined language, and a more structured premium positioning. This is usually better as a second-stage channel after one hero SKU proves repeat purchase.

The strongest growth model is often hybrid:

- Amazon for efficient hero-SKU validation

- DTC for education, bundles, and retention

- clinic or specialty channels later for premium expansion

Channel Strategy and Launch Timeline

Compliance and Claims Strategy

This category is highly sensitive to claim language. That is one of the biggest commercial realities of the U.S. hair growth market.

The core issue is simple: once claims move too far toward hair regrowth, treatment, or structure/function language, the product may move outside normal cosmetic territory.

For most cosmetic-support launches, the safer route is to use language such as:

- supports healthier-looking hair

- helps reduce breakage

- supports fuller-looking density

- supports scalp condition

- helps hair look thicker and stronger

- supports a healthier scalp environment

The higher-risk route is to use direct regrowth or treatment language without the appropriate regulatory pathway.

For this reason, the most important decision in product development often happens very early:

Is the product a cosmetic-support scalp treatment, or is it intended to operate as a true drug-positioned regrowth product?

That decision should govern claims, testing, packaging, and channel language from the start.

Quality and Testing Priorities

Hair growth products cannot rely on concept alone. They need a stronger operational foundation.

Suggested quality and development priorities include:

- stability testing

- microbial testing

- packaging compatibility

- leakage and transport assessment

- scalp irritation or dermatological compatibility review

- efficacy-supporting consumer perception or instrumental testing where needed

- applicator ergonomics and residue testing

Many launches fail not because the concept is wrong, but because the product is too greasy, too slow to apply, too difficult to understand, or too weak in early reinforcement signals.

In this category, long-term trust is built through use experience as much as through ingredient language.

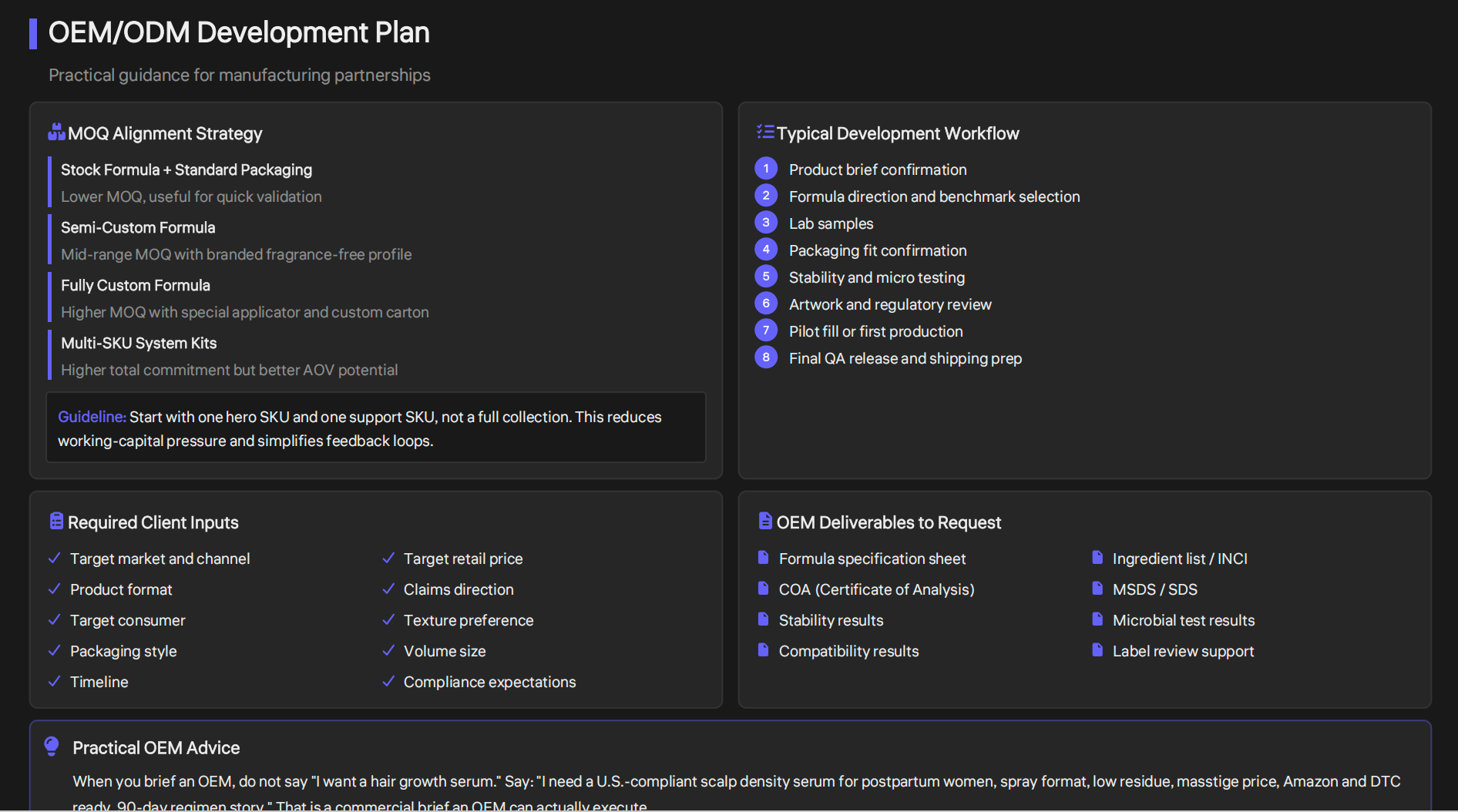

OEM Launch Opportunities

For OEM and private label development, the U.S. hair growth category offers real opportunity, but only when the brief is commercially usable.

A better OEM brief should define:

- target market

- lead consumer segment

- channel strategy

- product format

- claims boundary

- target price

- texture preference

- packaging system

- timeline

- compliance expectations

- first-order quantity

- 90-day regimen logic

When brands only ask for “a hair growth serum,” development becomes slower, less accurate, and more expensive. When brands define the real business case, the OEM can build toward launch reality rather than product guesswork.

A stronger example brief would be:

a U.S.-compliant postpartum scalp density tonic in spray format, low residue, masstige price tier, designed for Amazon and DTC, with a 90-day routine story.

That is the kind of brief that turns market insight into a product that can actually be quoted, sampled, and launched.

OEM/ODM Development Plan

What Brands Should Do Next

If you are planning to enter the U.S. hair growth market in 2026, the highest-probability strategy is this:

Start with one consumer problem, not a broad category story.

Launch one hero serum or tonic, not a large range.

Price the first product in masstige unless you already own premium authority.

Build the offer around 90-day routine adherence, not instant miracle language.

Use Amazon to validate the hero SKU and DTC to deepen education and retention.

Add support SKUs only after repeat purchase is proven.

This approach reduces risk, improves clarity, and gives the brand a much stronger chance of building a scalable assortment instead of a short-lived novelty launch.

Final Takeaway

The U.S. hair growth market in 2026 is attractive because it combines real emotional urgency with strong repeat-use potential. But it is not a category that rewards vague beauty positioning or reckless claims.

The brands most likely to win are the ones that combine believable positioning, disciplined claims, routine-friendly formats, clear channel fit, and a better retention model built around real consumer use cycles.

If your team is evaluating a hair growth launch, the strongest next step is to define the user problem, claim boundary, price band, and hero format first, then move into OEM briefing and sampling with a much clearer strategy.

Download the Full Report (PDF)

Tell us your target region, product category, and the decision you’re trying to make. We’ll suggest the closest existing report—or build a tailored version.