Executive Summary

This report explores the U.S. hair conditioner market in 2026, including format opportunities, pricing strategy, consumer demand, channel fit, compliance priorities, and OEM launch planning. It is designed to help brands, importers, distributors, and e-commerce sellers turn market insight into a more practical conditioner launch strategy.

U.S. Hair Conditioner Market Report 2026: Product Trends, Price Tiers, and OEM Launch Strategy

The U.S. hair conditioner market in 2026 is no longer driven by generic daily-care positioning alone. Growth is increasingly coming from premiumization, problem-specific routines, and products built around visible performance outcomes such as repair, hydration, frizz control, curl support, scalp comfort, and color-safe maintenance.

For brands, distributors, importers, and e-commerce sellers, this creates a more attractive but also more competitive market. The strongest opportunity is not to launch one conditioner for everyone. It is to build a focused product system around clear concerns, practical usage occasions, and price points that feel elevated without becoming inaccessible.

This report translates market signals into launch logic. It covers conditioner format opportunities, pricing strategy, channel fit, consumer demand, compliance priorities, and OEM execution planning for businesses entering or expanding in the U.S. conditioner category.

Executive Summary

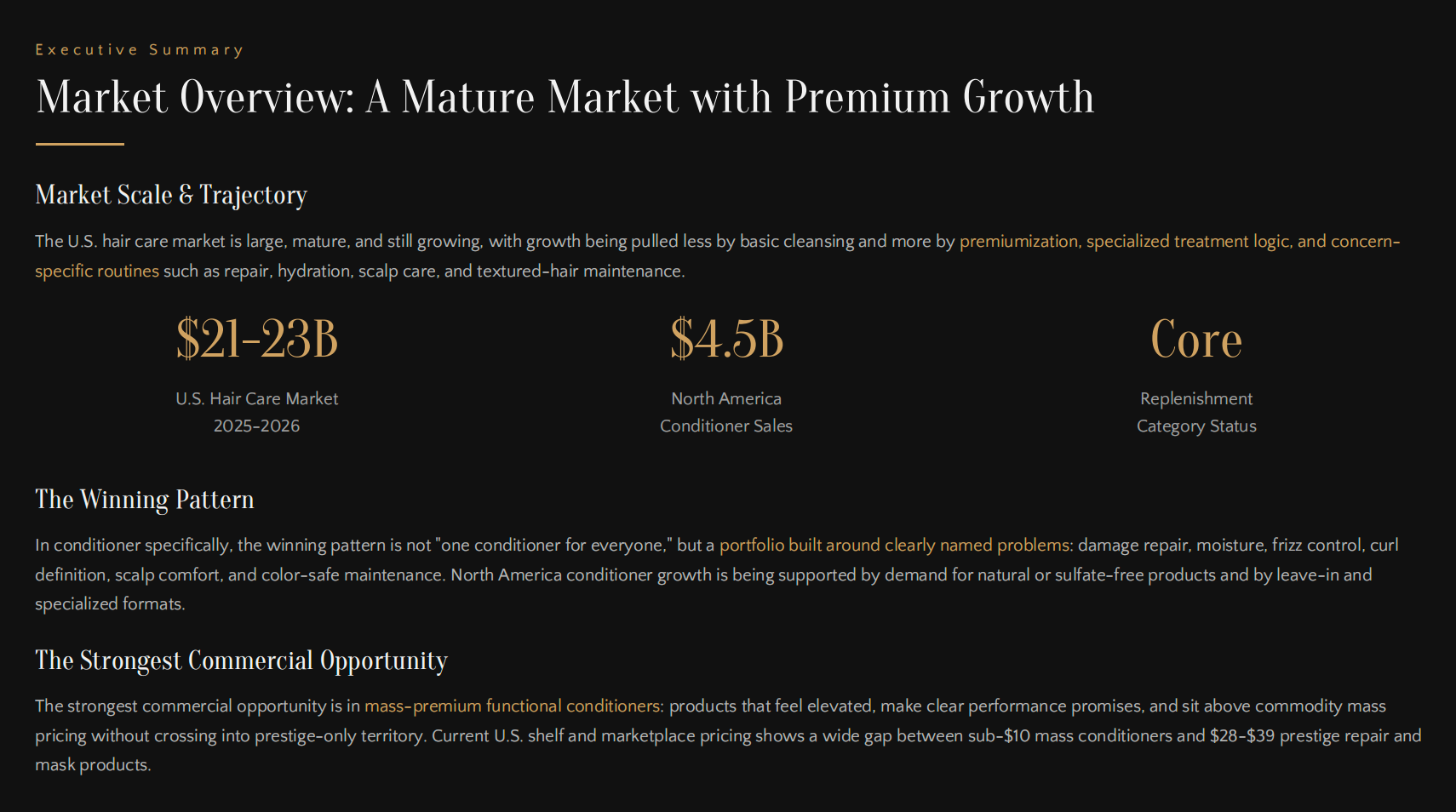

The U.S. conditioner category remains a core replenishment segment inside the broader hair care market, but the growth engine has shifted. Consumers are no longer buying conditioner only as a routine basic. They are buying for damage repair, softness, frizz reduction, detangling, moisture retention, scalp comfort, and texture-specific maintenance.

That means the strongest launches in 2026 are problem-led, not generic. A conditioner line performs better when each SKU has a clearly named use case, such as lightweight repair for fine hair, deep moisture for thick and frizz-prone hair, leave-in support for curls, or comfort-focused conditioning for sensitive scalp users.

For most new entrants, the best starting point is not an oversized portfolio. It is a compact system with one hero rinse-out conditioner, one leave-in, and one weekly mask, all built around one clear claim platform such as repair plus softness or hydration plus frizz control.

Market Opportunity Overview

The U.S. conditioner market sits inside a mature hair care environment, but it continues to generate attractive opportunities because consumers keep upgrading routines rather than simply buying less often. Conditioner is not an optional add-on. It is a repeat-purchase category tied to daily usability and visible hair feel.

What is changing is the reason people buy. Instead of asking only whether a conditioner is affordable or smells good, consumers increasingly ask whether it can help with a specific issue: breakage, roughness, tangling, dryness, frizz, curl definition, scalp tightness, or color-treated softness.

That shift makes the category commercially clearer. The brands most likely to win are not those with the broadest “for all hair types” message. They are the ones with sharper problem-solution positioning and a product structure that supports both replenishment and trade-up.

Market Overview: A Mature Market with Premium Growth

What Is Driving Demand in 2026

Several demand drivers are shaping the category.

The first is repair and strengthening. Consumers with bleached, heat-styled, or chemically treated hair continue to prioritize products that improve softness, reduce breakage feel, and support stronger-looking hair.

The second is hydration and frizz control. This remains one of the broadest demand zones, especially for consumers managing climate-related dryness, roughness, or flyaways.

The third is texture-led care. Curly and coily consumers often buy conditioner as part of a defined routine rather than a generic wash step, making leave-ins and masks especially important.

The fourth is scalp comfort. More shoppers want conditioning products that feel gentle, balancing, and lightweight, especially when dryness and scalp discomfort overlap.

The fifth is content-friendly functionality. Leave-ins, masks, and before-and-after formats are easier to explain in visual content, making them especially attractive for Amazon, DTC, and social-led commerce.

Consumer Demand Signals

The strongest commercial signals in the U.S. conditioner market point to a simple pattern: consumers may say they want clean, natural, or safer products, but they buy what clearly improves hair performance.

The highest-converting outcomes are:

- repair

- hydration

- softness

- frizz control

- detangling

- strengthening

- curl support

- color-safe maintenance

This means ingredient language works best as a trust layer rather than the main conversion driver. Sulfate-free, silicone-free, vegan, color-safe, or scalp-friendly can all help the product get shortlisted. But what usually closes the sale is visible payoff: smoother feel, easier comb-through, less frizz, more softness, or better curl behavior.

For product planning, the implication is clear. Formula design should start with hair performance and user experience first, then add cleaner or more reassurance-oriented filters where commercially helpful.

Core Consumer Segmentsœ

Conditioner Formats That Matter Most

The category is no longer defined by one rinse-out bottle alone. Several formats matter, and each plays a different business role.

Rinse-Out Conditioner

This remains the hero replenishment format for most brands. It supports repeat purchase, routine attachment, and easier bundle building. It should be the foundation SKU unless the brand is explicitly treatment-led.

Leave-In Conditioner

Leave-ins are especially strong for Amazon, DTC, and social content because they solve visible problems and are easier to demonstrate. They work particularly well for detangling, frizz control, curl moisture support, and heat-styled hair.

Deep Conditioner or Hair Mask

Masks are the clearest trade-up format in the category. They offer richer sensorial payoff, weekly ritual logic, and stronger perceived value. They are especially effective in repair and textured-hair lines.

Scalp-Friendly Conditioner

This is a developing opportunity. The strongest positioning here is not medical treatment language, but comfort, balance, softness, and light moisture.

Multifunction Conditioner

This is commercially relevant for convenience-led households, but it is usually not the strongest place for a new brand to establish expertise unless simplicity is the main value proposition.

Product Strategy: What to Formulate First

The best launch strategy is to build a compact but commercially structured portfolio.

A strong opening system usually includes:

- one hero rinse-out conditioner

- one leave-in conditioner

- one weekly mask

This structure works because it covers three different commercial needs at once:

- replenishment

- visible problem-solving

- trade-up value

For most entrants, the strongest claim platforms are:

- repair plus softness

- hydration plus frizz control

- curl support plus detangling

- lightweight moisture for fine hair

- scalp comfort plus softness

The key is not to launch too many variants too early. It is better to build one strong hero around a broad but clear concern, then add texture-specific or scalp-oriented extensions after the first system gains traction.

Recommended Launch Directions

A commercially effective first portfolio may include:

1. Daily Repair Conditioner

Built for damaged, color-treated, or heat-styled hair, with a medium cream texture and a clear repair plus softness promise.

2. Frizz Control Leave-In

Positioned for wavy, curly, or heat-styled users, with detangling, frizz control, and softness as the main outcomes.

3. Weekly Repair Mask

Designed for dry, damaged, or colored hair, giving richer texture payoff and stronger trade-up value.

This combination creates a balanced entry into the market because it covers routine use, visible content potential, and premium extension logic without forcing the brand into too many SKUs at launch.

Pricing Strategy

The U.S. conditioner market is clearly tiered, but one of the most attractive zones for new entrants is mass premium.

Entry Tier

Best for large-scale value and family-oriented positioning, but harder to defend for smaller brands without strong retail reach.

Mass Tier

Useful for accessible mainstream positioning, especially in replenishment-led channels, but still very competitive.

Mass Premium

This is often the best entry point for emerging brands. It allows better formula texture, stronger packaging, and healthier margins while remaining accessible enough for Amazon, DTC, and specialty beauty.

Premium

This tier works when the product has strong technology, salon credibility, founder authority, or enough content and reviews to justify conversion friction.

For many new brands, the most practical starting band is the mass-premium range, especially for repair, moisture, leave-in, and mask products.

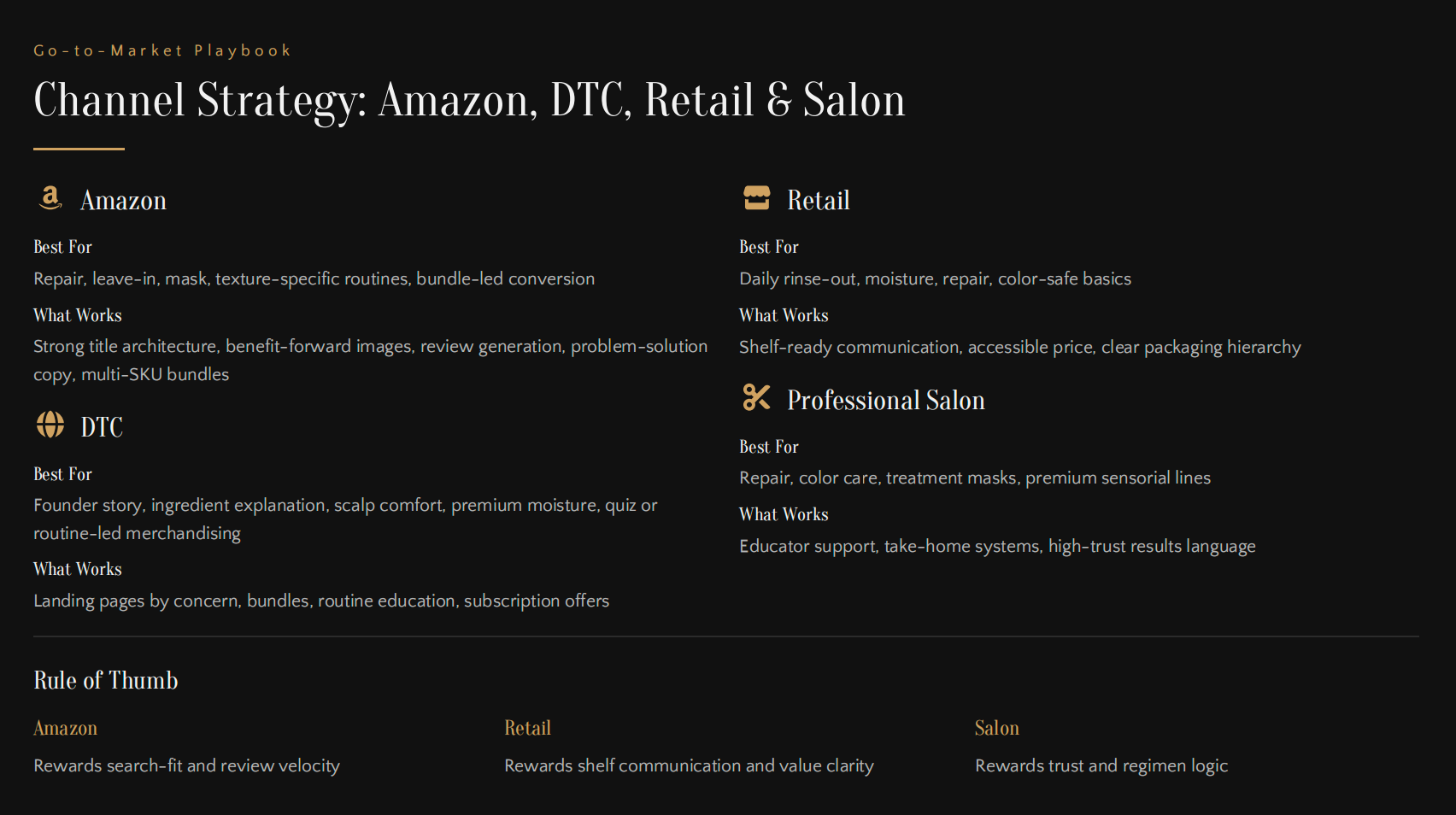

Channel Strategy

A conditioner launch should be channel-aware from the start.

Amazon

Amazon works especially well for leave-ins, repair systems, masks, and bundle-led conversion. Problem-solution titles, benefit-driven images, and review-building are critical.

DTC

DTC is strong for founder story, ingredient explanation, scalp-comfort positioning, premium moisture stories, and routine-led merchandising.

Retail

Retail is strongest for daily rinse-out, moisture, repair, and color-safe basics. Shelf communication and packaging clarity matter heavily.

Professional or Salon

This channel works best for repair, color care, treatment masks, and premium sensorial lines where trust and regimen logic matter.

The strongest strategy is not to push one identical product story across every channel. It is to adapt the assortment and messaging to how each channel actually converts.

Channel Strategy: Amazon, DTC, Retail & Salon

Bundle Strategy

Conditioner sells better when it is part of a routine. A good bundle system improves average order value, strengthens claim credibility, and makes the customer more likely to stay with the line.

Useful launch bundles include:

- repair duo

- repair trio

- frizz routine

- curl wash-day set

- mini discovery set

Bundle strategy should not be an afterthought. It should be designed into the launch plan from the beginning, especially for Amazon and DTC.

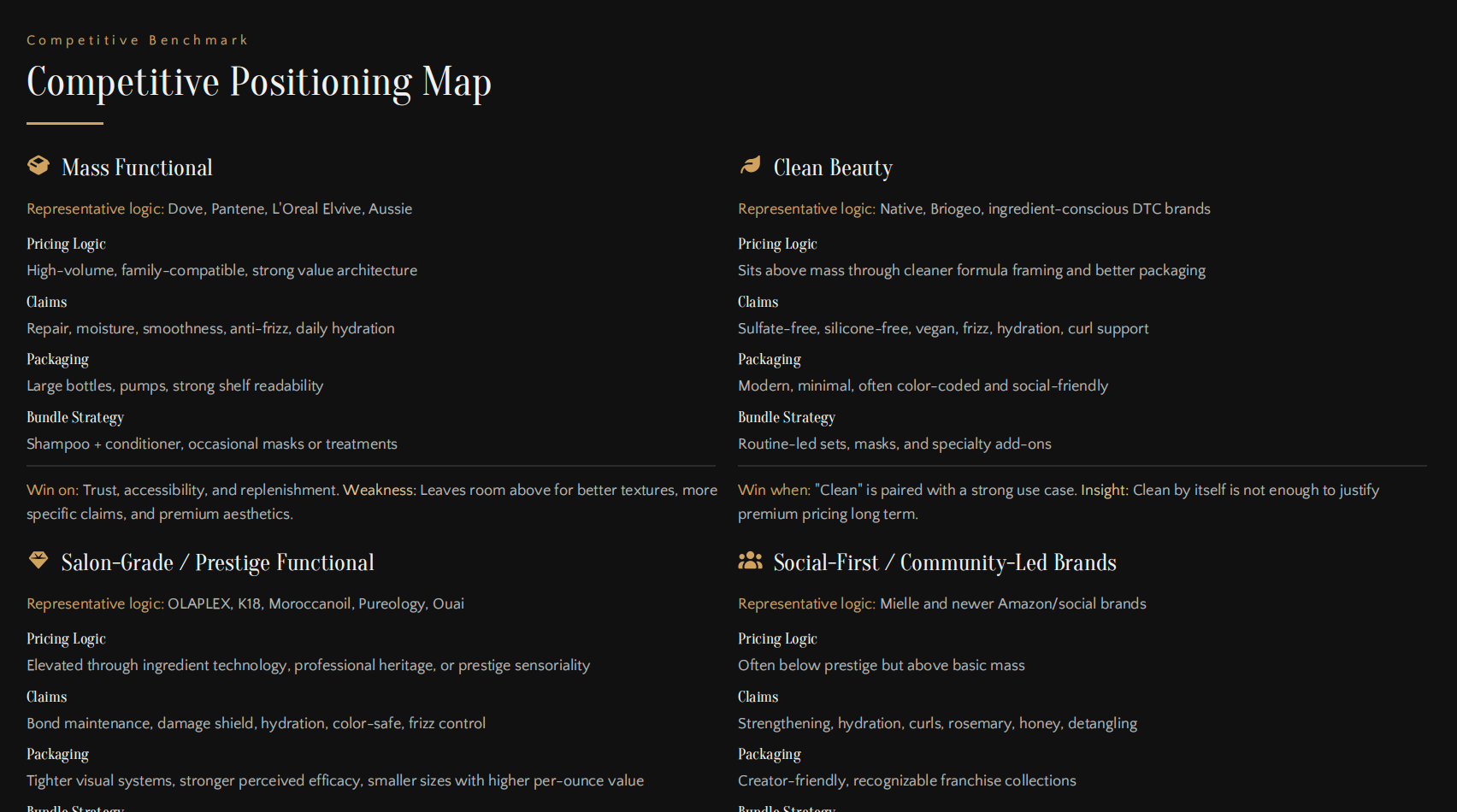

Competitive White Space

The market is crowded, but there are still clear opportunities.

The most attractive white spaces include:

- lightweight repair for fine or low-density hair

- scalp-comfort conditioner without a drugstore-medical feel

- mainstream-friendly leave-in for textured and frizz-prone hair

- color-safe moisture conditioner in the mass-premium range

- routine-first bundles designed for Amazon conversion

These are stronger entry points than launching another generic repair conditioner with no audience-specific angle.

Competitive Positioning Map

Compliance and Quality Priorities

Conditioner is often underestimated from a compliance perspective, but the risks are real.

The main priorities include:

- proper cosmetic labeling

- accurate ingredient declaration

- supportable claim language

- safety substantiation

- stability testing

- preservative robustness

- packaging compatibility

- disciplined use of “clean” language

- avoiding medical-style scalp claims when not appropriate

The safest commercial approach is to use specific, supportable language such as sulfate-free, silicone-free, color-safe, or dermatologist-tested only when those claims are properly supported. Generic “non-toxic” or overly broad safety claims can create unnecessary risk.

For a successful U.S. launch, compliance should be treated as part of product development, not post-launch paperwork.

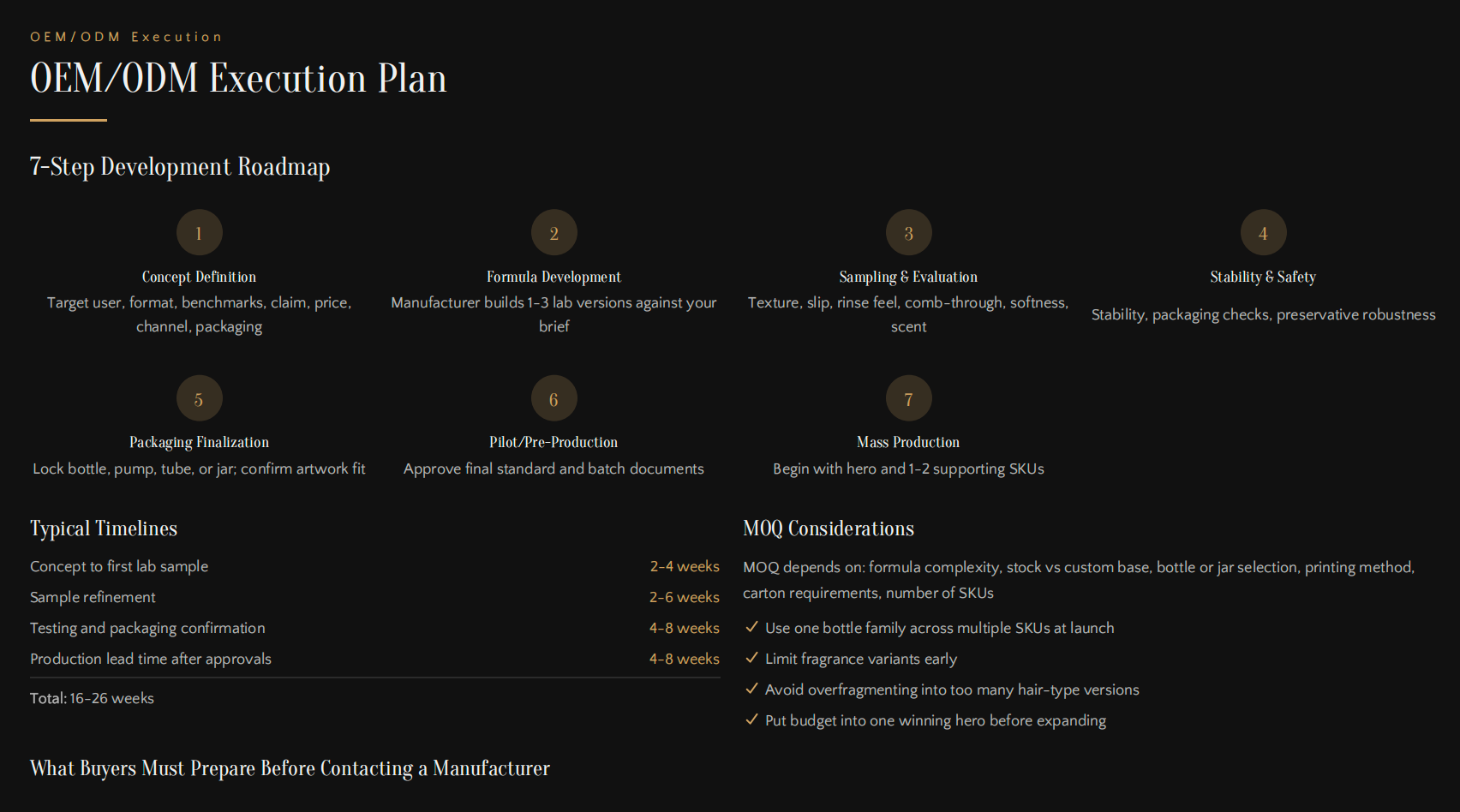

OEM and Launch Execution

The fastest way to reduce development waste is to brief the manufacturer more clearly from day one.

A stronger OEM brief should define:

- target market

- hero problem

- product format

- price band

- target channel

- benchmark products

- packaging direction

- launch timing

- required documents

- testing expectations

The more precise the brief, the faster the sampling process, the better the quote quality, and the lower the risk of endless reformulation rounds.

For most brands, the best execution path is:

- lock the hero formula first

- validate against benchmark products

- confirm packaging compatibility

- launch only two or three SKUs first

- expand after learning which claim truly converts

That approach is safer, clearer, and easier to scale.

OEM/ODM Execution Plan

Final Takeaway

The U.S. hair conditioner market in 2026 remains attractive, but the winning logic has changed. Consumers no longer reward generic conditioning promises the way they once did. They are buying solutions for damage, dryness, frizz, texture, softness, and scalp comfort.

The brands most likely to win are not the ones launching the most products. They are the ones building the clearest product system: one strong hero, one visible problem-solving extension, one trade-up format, and one channel-aware pricing structure.

If you are planning a conditioner launch for the U.S. market, the strongest next step is to define the problem you solve, the format that proves it, the price band that fits your channel, and the OEM path that can execute it cleanly.

Download the Full Report (PDF)

Tell us your target region, product category, and the decision you’re trying to make. We’ll suggest the closest existing report—or build a tailored version.