Executive Summary

This report explores the EU men’s fragrance market in 2026, including market size, demand shifts, scent and format trends, price architecture, channel strategy, compliance priorities, and private label launch opportunities. It is designed to help brand owners, distributors, Amazon sellers, DTC operators, and product development teams turn market insight into a more practical fragrance launch plan.

EU Men’s Fragrance Market 2026: Trends, Size, and Private Label Launch Opportunities

The EU men’s fragrance market in 2026 offers a meaningful growth opportunity for brands, distributors, e-commerce sellers, and private label buyers looking for scalable fragrance programs with stronger positioning and better format strategy.

The market is no longer moving in one single direction. It is splitting into two winning poles: accessible prestige with broader conversion potential, and higher-concentration premium fragrances with stronger storytelling, higher margins, and niche-inspired appeal.

For buyers planning a new launch, the opportunity is not just to enter the category with another generic men’s cologne. The stronger path is to build a disciplined fragrance system with the right hero scent, the right trial format, the right concentration ladder, and the right compliance and packaging execution.

This report translates the EU men’s fragrance opportunity into practical launch logic. It covers market size, demand shifts, format trends, category structure, private label whitespace, compliance priorities, and OEM execution planning for 2026.

Executive Summary

The EU men’s fragrance market remains one of the most attractive fragrance segments for commercial entry in 2026. It combines scale, premiumization, format innovation, and room for fast private label response.

The strongest growth is not coming from one price tier alone. Consumers are rewarding both accessible premium offers and more concentrated premium or niche-inspired fragrances. At the same time, buyers are showing more interest in portable formats, body sprays, travel sizes, and discovery-led entry points that reduce risk and improve first purchase conversion.

For most new entrants, the strongest launch path is not a large assortment. It is a focused product architecture:

-

one hero men’s EDP

-

one lower-commitment entry format

-

one higher-margin premium concentration or refillable upgrade

This creates a more commercially usable price ladder while keeping development, packaging, and channel execution under control.

Market Opportunity Overview

The EU remains one of the most valuable fragrance regions in the world, with a strong retail base, established premium infrastructure, and multiple country-level opportunities across Western, Southern, and selected Eastern markets.

For men’s fragrance specifically, the opportunity is large enough for scale but fragmented enough for targeted positioning. That makes it well suited to private label entry, especially for brands and distributors that want a more flexible route than legacy fragrance houses can usually provide.

What matters in 2026 is not simply participating in fragrance growth. What matters is launching into the right sub-space:

-

performance-led men’s scents

-

accessible premium price bands

-

stronger-concentration formats

-

portable discovery formats

-

modern masculine profiles that move beyond generic blue-fragrance positioning

Market Snapshot

What Is Driving Demand in 2026

Several shifts are shaping the EU men’s fragrance market.

The first is premiumization. Fragrance remains one of the most accessible ways for consumers to buy identity, status, and self-expression without entering full luxury spending.

The second is fragrance as identity. Men increasingly use fragrance not only as a grooming product, but as part of image, mood, social signaling, and occasion-based self-presentation.

The third is performance expectation. Consumers are paying more attention to longevity, projection, and concentration level, especially in online reviews and niche-inspired launches.

The fourth is format innovation. Body sprays, travel sizes, sample sets, and layering formats are making fragrance easier to try, gift, and repurchase.

The fifth is social discovery. Fragrance trends now move faster because of TikTok, Instagram, creator-led reviews, and digital scent storytelling.

Consumer Demand Signals

The most important buyer groups in the EU men’s fragrance market include younger men using fragrance as identity and experimentation, millennials seeking confidence and premium self-reward, and core male fragrance buyers in the 21–40 age range who drive scalable volume.

Their main purchase motivations are consistent:

-

to smell attractive and feel confident

-

to signal taste, lifestyle, or status

-

to own multiple scents for different occasions

-

to access premium feeling without full niche pricing

-

to try before committing to a full bottle

This means brands should stop building products around broad category labels only. A more effective route is to brief products by use occasion:

-

office

-

date night

-

gym or fresh reset

-

evening or winter wear

-

travel and reapply

That structure gives the product line clearer commercial roles and makes channel planning easier.

Scent and Format Trends with the Strongest Potential

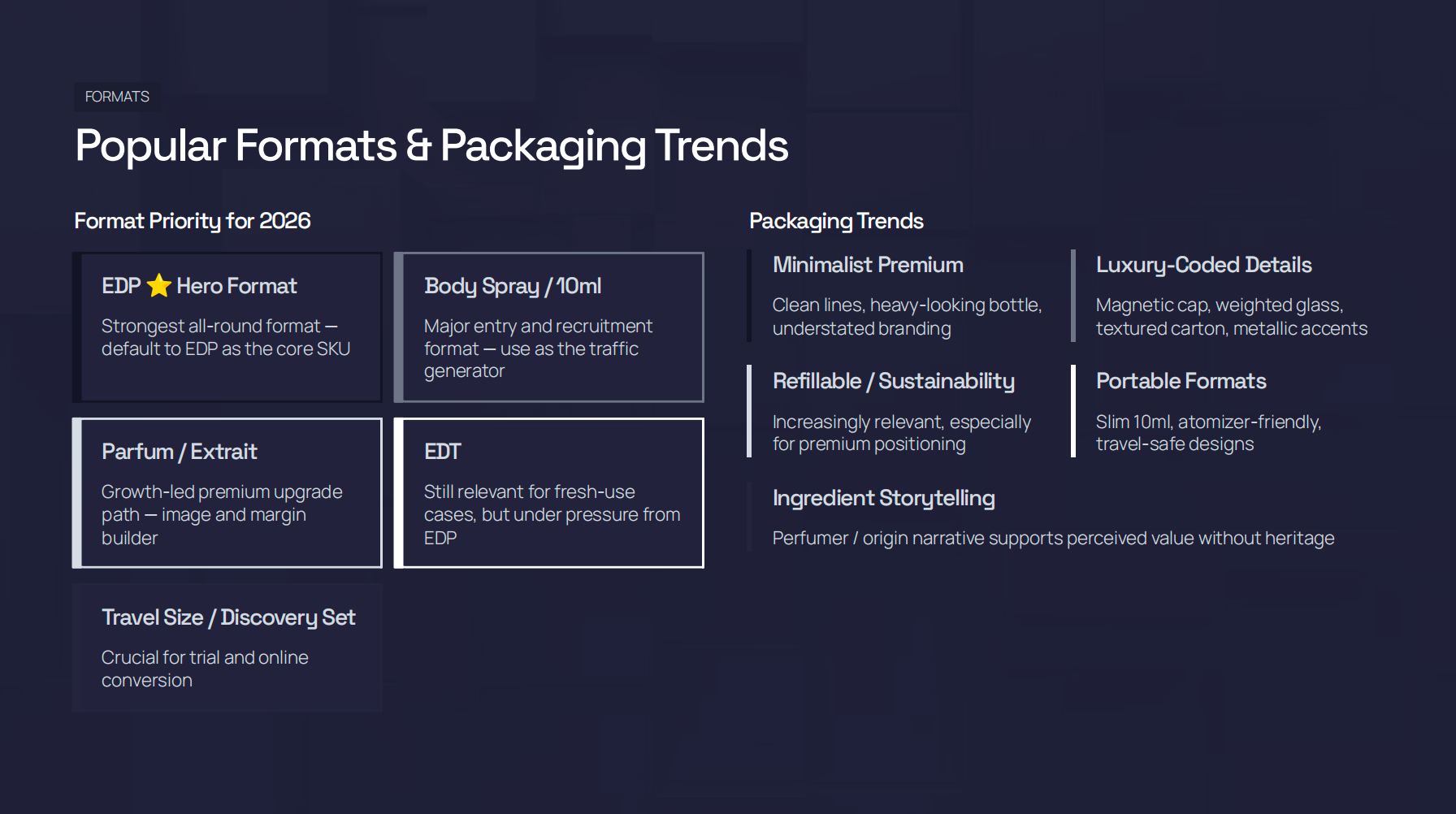

The strongest 2026 men’s fragrance launches in the EU are not simply “fresh men’s EDTs.” The category is moving toward better-performing formats and more differentiated scent stories.

The strongest opportunities include:

-

woody amber EDP

-

fresh aromatic men’s EDP

-

oud-musk and smoky evening scents

-

amber vanilla performance-led fragrances

-

clean skin musk layering scents

-

marine mineral freshwear formats

-

body spray recruitment products

-

10ml and 15ml travel sizes

-

discovery trios and trial sets

-

extrait or premium refillable upgrades

For most brands, EDP should be the hero format. Body spray or 10ml travel formats work well as the entry point, while extrait or refillable premium EDP can act as the image and margin builder.

Popular Formats & Packaging Trends

Category Landscape and Price Ladder

The EU men’s fragrance market is clearly segmented, but the best commercial opportunities are often found in the spaces between extremes.

A practical price ladder looks like this:

Entry / Accessible

-

body spray

-

small EDT

-

trial formats

-

youth recruitment and impulse buying

Mid / Accessible Premium

-

core men’s EDP

-

better-performing everyday fragrances

-

strongest fit for Amazon, DTC, gifting, and repeat purchase

Premium

-

higher-oil EDP

-

better bottle, cap, and carton

-

stronger selective retail and boutique potential

Niche-Inspired Premium

-

extrait or parfum

-

deeper scent architecture

-

higher gross margin but narrower audience

For most private label launches, the strongest path is not to compete at the very bottom or the extreme niche end first. It is to enter through accessible premium, then extend upward.

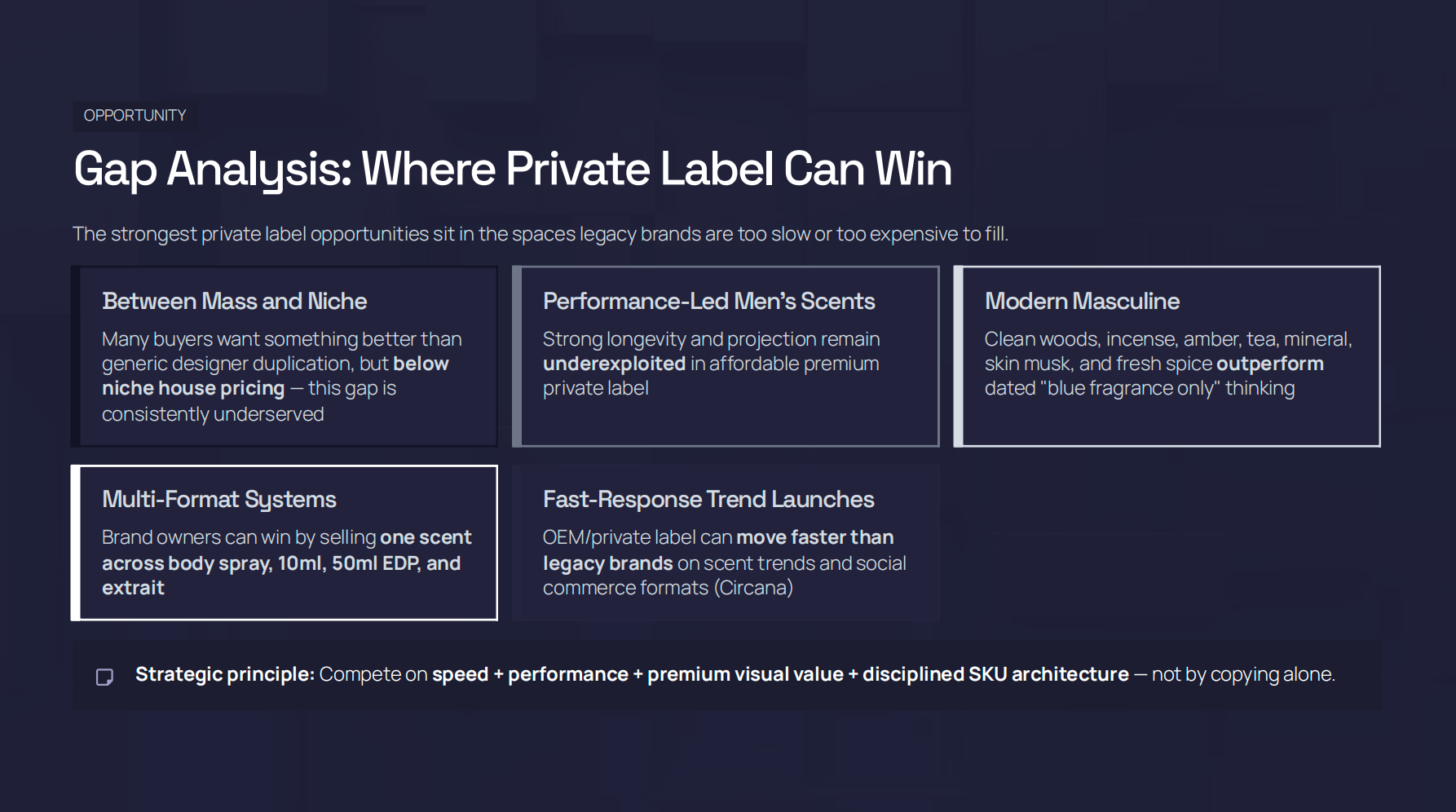

Where Private Label Can Win

Private label does not need to win by copying designer brands too closely. The better opportunity sits in the space between mass familiarity and niche aspiration.

The strongest private label whitespace includes:

-

better-than-mass performance at mid-tier pricing

-

premium visual value without full luxury cost

-

men’s scents with stronger longevity and projection

-

modern masculine profiles that avoid dated tropes

-

multi-format systems built around one core scent

-

faster-response trend launches for social commerce and DTC

This is where private label has a real edge. It can move faster than legacy brands, build more disciplined SKU systems, and bring premium-looking products to market without the weight of luxury-house overhead.

Gap Analysis: Where Private Label Can Win

High-Potential Product Directions

A practical 2026 assortment should not start with too many fragrances. It should begin with a focused mix that serves different roles.

A strong product mix may include:

-

one everyday fresh woody EDP

-

one long-lasting amber vanilla EDP

-

one premium oud or smoky night concentration

-

one marine or mineral freshwear entry product

-

one clean skin-musk layering scent

-

one body spray for recruitment and repeat use

-

one 10ml discovery trio for low-risk trial

-

one refillable signature EDP for premium image building

The hero launch candidates are usually the broad-appeal EDPs. The entry traffic drivers are body spray and discovery formats. The premium margin builders are extrait and refillable premium SKUs.

Channel Strategy

A strong men’s fragrance launch should be channel-aware from the start.

Amazon

Amazon works best for:

-

broad-appeal EDPs

-

performance-led positioning

-

travel or discovery formats

-

review-friendly scent families

Winning products need clear scent-family language, strong visual differentiation, and packaging that performs well in e-commerce environments.

Retail

Retail works best for:

-

giftable packaging

-

broad scent acceptance

-

clean price ladders

-

easy-to-understand scent positioning

Shelf performance matters here, so packaging execution and scent accessibility are especially important.

DTC

DTC works best for:

-

story-led launches

-

niche-coded branding

-

sampling ladders

-

bundle offers

-

content around mood, identity, and layering

This is often the best place to test format systems and collect first-party data.

Distributors and Importers

This route works best for:

-

regional rollouts

-

private label adaptation

-

country-by-country format strategy

-

scalable documentation and labeling workflows

The strongest offer here is a modular OEM fragrance system rather than one rigid SKU set.

Gap Analysis: Where Private Label Can Win

Compliance and Risk Priorities

In the EU men’s fragrance market, compliance is not a side issue. It directly affects launch readiness and long-term viability.

Key priorities include:

-

allergen labeling accuracy

-

formula lock before artwork finalization

-

CPNP-related documentation workflows

-

IFRA-aligned support documents

-

stability and compatibility testing

-

leakage and pack performance testing

-

bottle, pump, and cap compatibility

-

margin control through disciplined packaging choices

Many launch problems are not caused by poor scent ideas. They are caused by artwork delays, incompatibility between juice and pack, stability failures, or overbuilt packaging that erodes margin.

The strongest operators treat compliance, stability, and packaging as part of product strategy from the beginning.

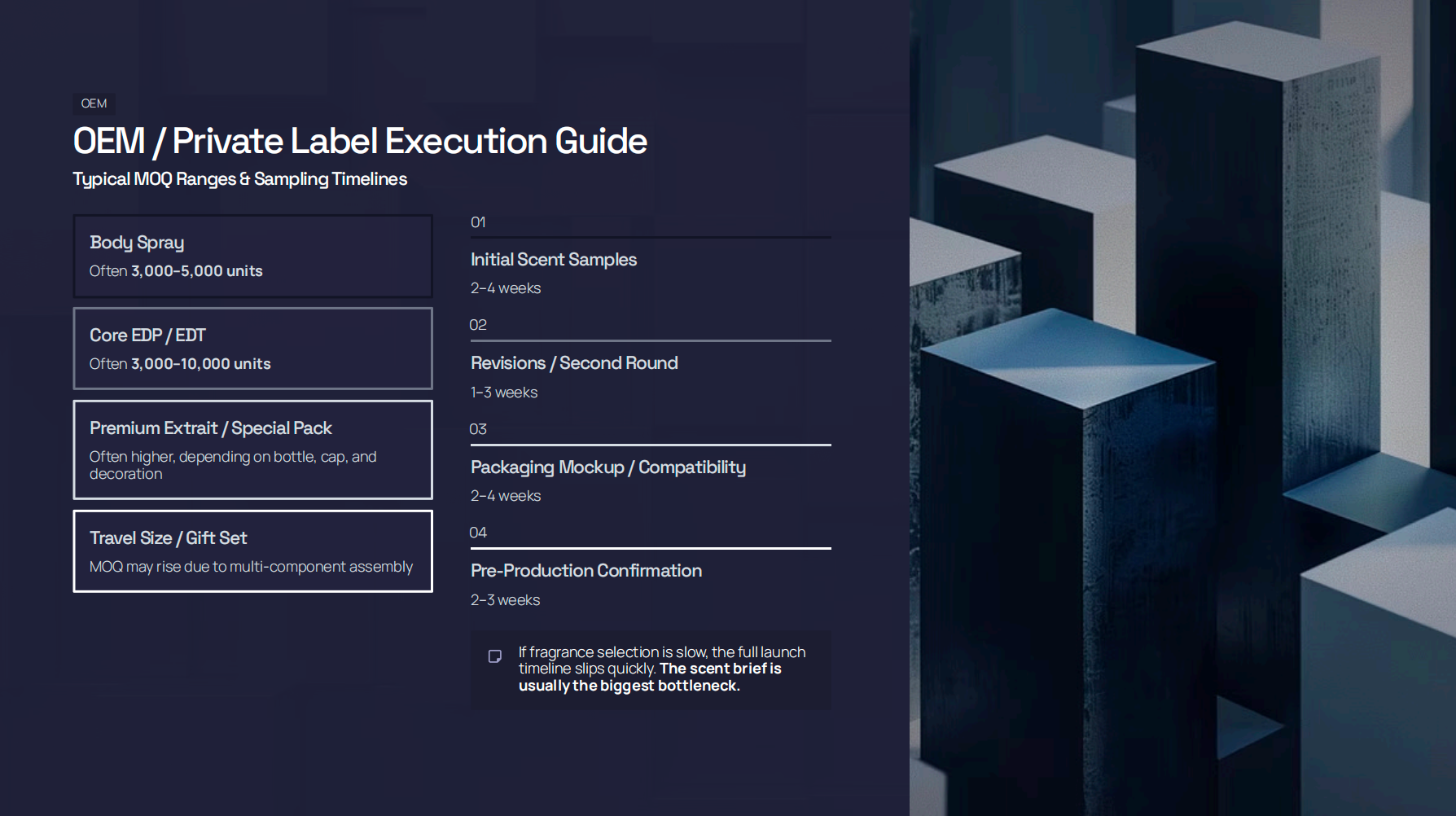

OEM / Private Label Execution Guide

The fastest way to improve development quality is to submit a better brief.

A stronger OEM brief should include:

-

scent direction

-

target retail price

-

channel

-

target user

-

use occasion

-

packaging style

-

performance expectation

-

hero size

-

entry format

-

premium extension plan

-

required documents

-

sampling timeline

-

launch deadline

It is also useful to ask suppliers for:

-

a good version

-

a better version

-

a best version

This helps teams compare cost, performance, and visual value without getting stuck between “too basic” and “too expensive.”

A good OEM partner should support not only formula filling, but also scent direction alignment, price architecture, packaging compatibility, documentation readiness, and practical launch sequencing.

OEM / Private Label Execution Guide

What Buyers Should Do Next

If you are planning an EU men’s fragrance launch, the smartest next step is not to begin with too many scent concepts at once.

A more effective sequence is:

-

freeze one hero scent first

-

define one acquisition format

-

define one premium margin-builder

-

validate scent direction with real target buyers

-

lock formula before artwork

-

test full packaging compatibility before bulk production

-

build the assortment around channel fit, not internal preference only

This reduces wasted development time and creates a stronger commercial foundation.

Final Takeaway

The EU men’s fragrance market in 2026 offers a real, scalable opportunity for brand owners, distributors, e-commerce sellers, and product development teams that want a private label route into fragrance.

The strongest entrants will not be the ones launching the most SKUs. They will be the ones launching the right architecture:

-

one hero men’s EDP

-

one sampling or entry product

-

one premium margin builder

-

one clear price ladder

-

one disciplined execution path

Winning in 2026 will come from the right scent, the right concentration, the right packaging level, and the right commercial focus.

Download the Full Report (PDF)

Tell us your target region, product category, and the decision you’re trying to make. We’ll suggest the closest existing report—or build a tailored version.